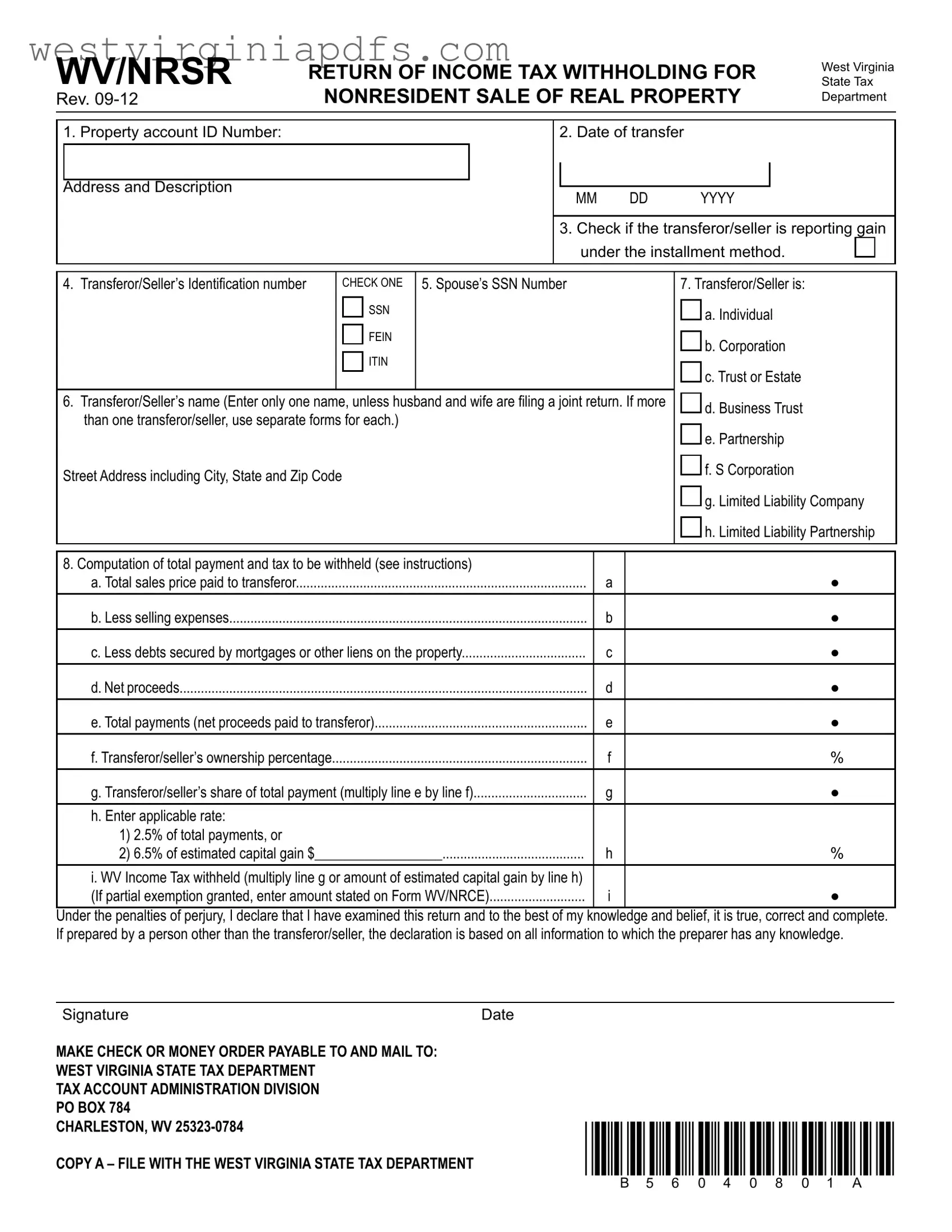

Fill Out a Valid Wv Nrsr Form

In the intricate landscape of real estate transactions, the WV/NRSR Return of Income Tax Withholding for Nonresident Sale of Real Property holds a pivotal role for ensuring compliance with West Virginia State Tax laws, specifically tailored for nonresident individuals or entities engaging in the sale of real property within the state. This form serves as a conduit for the state to secure its due taxes at the time of property transfer, streamlining the process for both the transferor and the state. Precisely designed, it requires detailed information about the property transaction, including identification numbers, dates, and the financial breakdown of the sale. A unique aspect is its accommodation for various transferor types, from individuals to trusts, each with its designated reporting requirements. The form meticulously outlines the computation of the applicable withholding tax based on the total payment or estimated capital gains, ensuring an accurate reflection of the tax obligations. Furthermore, it highlights the essential step of submitting the appropriate copy of the form alongside the necessary payment to the West Virginia State Tax Department, thus finalizing the process. Not only does it facilitate a smoother transition of property ownership but also emphasizes the importance of transparency and adherence to state tax regulations. Compliance with this requirement underscores a critical checkpoint in the nonresident property sale process, reflecting the broader commitment to ensuring that all participants contribute fairly to the state’s fiscal health.

Sample - Wv Nrsr Form

WV/NRSR |

RetuRN of iNcome tax WithholdiNg foR |

Rev. |

NoNReSideNt Sale of Real pRopeRty |

West Virginia

State Tax

Department

|

1. Property account ID Number: |

|

|

|

|

|

2. Date of transfer |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address and Description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MM |

DD |

|

|

YYYY |

|||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Check if the transferor/seller is reporting gain |

||||||||

|

|

|

|

|

|

|

|

under the installment method. |

|

|

|||||

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

4. Transferor/Seller’s Identiication number |

|

CheCk one |

5. Spouse’s SSN Number |

|

|

7. Transferor/Seller is: |

||||||||

|

|

|

|

SSn |

|

|

|

|

|

|

|

a. Individual |

|||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

FeIn |

|

|

|

|

|

|

|

b. Corporation |

|||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ITIn |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

c. Trust or Estate |

||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

6. Transferor/Seller’s name (Enter only one name, unless husband and wife are iling a joint return. If more |

|

|

d. Business Trust |

|||||||||||

|

|

|

|||||||||||||

|

than one transferor/seller, use separate forms for each.) |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

e. Partnership |

|||||||||

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Street Address including City, State and Zip Code |

|

|

|

|

|

|

|

|

|

f. S Corporation |

||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

g. Limited Liability Company |

|||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

h. Limited Liability Partnership |

|||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

8. Computation of total payment and tax to be withheld (see instructions) |

|

|

|

|

|

|

|

|

|

|||||

|

a. Total sales price paid to transferor |

|

|

|

|

|

|

a |

|

|

|

● |

|||

|

b. Less selling expenses |

|

|

|

|

|

|

b |

|

|

|

● |

|||

|

c. Less debts secured by mortgages or other liens on the property |

|

c |

|

|

|

|

● |

|||||||

|

d. Net proceeds |

|

|

|

|

|

|

d |

|

|

|

● |

|||

|

e. Total payments (net proceeds paid to transferor) |

|

|

e |

|

|

|

● |

|||||||

|

f. Transferor/seller’s ownership percentage |

|

|

|

|

|

|

f |

% |

|

|

||||

|

g. Transferor/seller’s share of total payment (multiply line e by line f) |

|

|

g |

|

|

|

● |

|||||||

|

h. Enter applicable rate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1) 2.5% of total payments, or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2) 6.5% of estimated capital gain $__________________ |

|

|

h |

% |

|

|

||||||||

|

i. WV Income Tax withheld (multiply line g or amount of estimated capital gain by line h) |

|

|

|

|

|

|

|

|||||||

|

(If partial exemption granted, enter amount stated on Form WV/NRCE) |

|

|

i |

|

|

|

● |

|||||||

Under the penalties of perjury, I declare that I have examined this return and to the best of my knowledge and belief, it is true, correct and complete. If prepared by a person other than the transferor/seller, the declaration is based on all information to which the preparer has any knowledge.

Signature |

Date |

|

Make check or Money order payable to and Mail to: |

|

|

West Virginia state tax departMent |

|

|

tax account adMinistration diVision |

|

|

po box 784 |

|

|

charleston, WV |

*b56040801a* |

|

copy a – File With the West Virginia state tax departMent |

||

|

WV/NRSR

InstructIons for return of Income tax wIthholdIng

for nonresIdent sale of real property

here are three copies of From WV/NRSR

GeNeRal INStRuctIoNS

Purpose of form:

his form is designed to assure the regular and timely collection of wV income tax due from nonresident sellers of real property located within the state. his form is used to determine the amount of income tax withholding due on the sale of property and provide for its collection at the time of the sale or transfer.

Who must file:

If the transferor/seller is a nonresident individual or nonresident entity, and is transferring an interest in real property located within the state of wV, unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must ile form wV/nrsr with the wV state tax department. If there are multiple transferors/sellers, a separate form must be completed for each nonresident individual or nonresident entity subject to the withholding requirements. he separate form requirement does not apply to a husband and wife iling a joint wV income tax return.

a “nonresident entity” is deined to mean an entity that: (1) is not formed under the laws of wV, and (2) is not qualiied by or registered with the wV state tax department to do business in wV.

When to file:

unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must complete form wV/nrsr for each nonresident transferor/seller at closing of sale.

a nonresident individual or nonresident entity that sells real or personal property located in wV must ile a wV income tax return. he appropriate income tax return must be iled for the year in which the transfer of the real property occurred. he due date for each income tax return type can be found in the instructions to the speciic income tax return.

What to file:

copy a of form wV/nrsr must be submitted to the wV state tax department with check or money order in the aggregate amount of tax due for each nonresident transferor/seller with regard to a sale or transfer of real property within thirty (30) days of the date the amounts were withheld.

copy B of form wV/nrsr is to be provided to the transferor/seller at closing. nonresident individuals or nonresident entities must ile the appropriate wV income tax return for the year in which the transfer of the property occurred. see the speciic instructions for the tax return being iled.

copy c of form wV/nrsr is to be retained by the taxpayer.

SpecIfIc INStRuctIoNS foR completING the foRm:

lIne 1 enter the street address for the property as listed with the county assessor. If the property does not have a street address, provide such descriptive information as is used by the county assessor to identify the property. also include the property account Id number for the parcel being transferred. If the property is made up of more than one parcel and has more than one account number, include all applicable account numbers.

lINe 2 enter the date of transfer. he date of transfer is the efective date of the deed. he efective date is the later of: (1) the date of the last acknowledgement; or (2) the date stated in the deed.

lINe 3 check the box if the transferor/seller is reporting the gain under the installment method.

lINeS 4, 5, and 6 unless transferors/sellers are husband and wife and iling a joint wV income tax return, a separate form wV/ nrsr must be completed for each transferor/seller that is entitiled to receive any part of the proceeds of the transfer. enter the tax identiication number or social security number for the nonresident transferor/seller and the social security number for the spouse, if applicable. do not enter the street address of the property being transferred.

lINe 7 check the appropriate box for the transferor/seller.

lINe 8 If a certiicate of partial exemption is issued by the wV state tax commissioner, do not complete lines 8a through 8h. Instead, enter the amount stated on form wV/nrce.

complete this section to determine the total payment allocable to the transferor/seller that is subject to the income tax withholding requirements and the amount of tax required to be withheld. he total payment is computed by deducting from the total sales price including the fair market value of any property or other non- monetary consideration paid to or otherwise transferred to the transferor/seller the amount of any mortgages or other liens, the commission payable on account of the sale, and any other expenses due from the seller in connection with the sale.

lINe 8f If there are multiple owners, enter the percentage of ownership of the transferor/seller for whom this form is being iled.

lINe 8g multiply line 8e by line 8f to determine the transferor/ seller’s share of the total payment.

lINe 8h enter the applicable rate for the transferor/seller used for computing the withholding tax. If withholding tax is computed on 6.5%, enter the amount of the estimated capital gain on line h2.

lINe 8i enter the amount of tax withheld.

payment of tax: make check or money order payable to the wV state tax department.

signature: copy a of this return must be veriied and signed by the individual transferor/seller, an authorized person or oicer of a business entity, or the person responsible for closing.

SpecIfIc INStRuctIoNS foR tRaNSfeRoR/SelleR (copy B)

How to claim the tax withheld

a copy of form wV/nrsr (copy B) must be submitted with the appropriate wV Income tax return. failure to do so will result in

the disallowance of the credit claimed.

he manner in which the income tax withheld is claimed by the nonresident individual or nonresident entity depends on the type of wV income tax return you are required to ile. follow the speciic instructions below. claiming the income tax withheld on a line other than as described below may result in the withholding being denied.

Individuals and Revocable Living Trusts

nonresident individuals are required to ile a nonresident wV Income tax return (form

C corporations

c corporations are required to ile a wV combined corporation net Income/Business franchise tax return (form wV/cnf120).

he income tax withheld and reported on line 8 of form wV/nrsr must be claimed as a withholding income tax payment.

S corporations, Partnerships and Limited Liability Companies and Business Trusts

s corporation, partnerships and limited liability companies and business trusts that elect to be treated as

his tax, and any other tax paid with form wV/nrsr must be allocated to the nonresident shareholders, partners or members and reported on a modiied federal schedule

Trusts and Estates

trustees of trusts and personal representatives of estates are required to ile a wV fiduciary Income tax return (form

WV/NRSR |

RetuRN of iNcome tax WithholdiNg foR |

Rev. |

NoNReSideNt Sale of Real pRopeRty |

West Virginia

State Tax

Department

|

1. Property account ID Number: |

|

|

|

|

|

2. Date of transfer |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address and Description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MM |

|

DD |

|

|

YYYY |

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Check if the transferor/seller is reporting gain |

||||||||||

|

|

|

|

|

|

|

|

under the installment method. |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

4. Transferor/Seller’s Identiication number |

|

CheCk one |

5. Spouse’s SSN Number |

|

|

|

7. Transferor/Seller is: |

|||||||||

|

|

|

|

SSn |

|

|

|

|

|

|

|

|

|

a. Individual |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

FeIn |

|

|

|

|

|

|

|

|

|

b. Corporation |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ITIn |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

c. Trust or Estate |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

6. Transferor/Seller’s name (Enter only one name, unless husband and wife are iling a joint return. If more |

|

|

d. Business Trust |

|||||||||||||

|

|

|

|||||||||||||||

|

than one transferor/seller, use separate forms for each.) |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

e. Partnership |

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Street Address including City, State and Zip Code |

|

|

|

|

|

|

|

|

|

|

|

f. S Corporation |

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

g. Limited Liability Company |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

h. Limited Liability Partnership |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

8. Computation of total payment and tax to be withheld (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

a. Total sales price paid to transferor |

|

|

|

|

|

|

|

a |

|

|

|

|

● |

|||

|

b. Less selling expenses |

|

|

|

|

|

|

|

b |

|

|

|

|

● |

|||

|

c. Less debts secured by mortgages or other liens on the property |

|

c |

|

|

|

|

|

|

● |

|||||||

|

d. Net proceeds |

|

|

|

|

|

|

|

d |

|

|

|

|

● |

|||

|

e. Total payments (net proceeds paid to transferor) |

|

|

|

e |

|

|

|

|

● |

|||||||

|

f. Transferor/seller’s ownership percentage |

|

|

|

|

|

|

|

f |

|

% |

|

|

||||

|

g. Transferor/seller’s share of total payment (multiply line e by line f) |

|

|

|

g |

|

|

|

|

● |

|||||||

|

h. Enter applicable rate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1) 2.5% of total payments, or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2) 6.5% of estimated capital gain $__________________ |

|

|

|

h |

|

% |

|

|

||||||||

|

i. WV Income Tax withheld (multiply line g or amount of estimated capital gain by line h) |

|

|

|

|

|

|

|

|

|

|||||||

|

(If partial exemption granted, enter amount stated on Form WV/NRCE) |

|

|

|

i |

|

|

|

|

● |

|||||||

copy b – For transFeror/seller(records copy)

WV/NRSR |

RetuRN of iNcome tax WithholdiNg foR |

Rev. |

NoNReSideNt Sale of Real pRopeRty |

West Virginia

State Tax

Department

|

1. Property account ID Number: |

|

|

|

|

|

2. Date of transfer |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address and Description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MM |

|

DD |

|

|

YYYY |

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Check if the transferor/seller is reporting gain |

||||||||||

|

|

|

|

|

|

|

|

under the installment method. |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

4. Transferor/Seller’s Identiication number |

|

CheCk one |

5. Spouse’s SSN Number |

|

|

|

7. Transferor/Seller is: |

|||||||||

|

|

|

|

SSn |

|

|

|

|

|

|

|

|

|

a. Individual |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

FeIn |

|

|

|

|

|

|

|

|

|

b. Corporation |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ITIn |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

c. Trust or Estate |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

6. Transferor/Seller’s name (Enter only one name, unless husband and wife are iling a joint return. If more |

|

|

d. Business Trust |

|||||||||||||

|

|

|

|||||||||||||||

|

than one transferor/seller, use separate forms for each.) |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

e. Partnership |

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Street Address including City, State and Zip Code |

|

|

|

|

|

|

|

|

|

|

|

f. S Corporation |

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

g. Limited Liability Company |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

h. Limited Liability Partnership |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

8. Computation of total payment and tax to be withheld (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

a. Total sales price paid to transferor |

|

|

|

|

|

|

|

a |

|

|

|

|

● |

|||

|

b. Less selling expenses |

|

|

|

|

|

|

|

b |

|

|

|

|

● |

|||

|

c. Less debts secured by mortgages or other liens on the property |

|

c |

|

|

|

|

|

|

● |

|||||||

|

d. Net proceeds |

|

|

|

|

|

|

|

d |

|

|

|

|

● |

|||

|

e. Total payments (net proceeds paid to transferor) |

|

|

|

e |

|

|

|

|

● |

|||||||

|

f. Transferor/seller’s ownership percentage |

|

|

|

|

|

|

|

f |

|

% |

|

|

||||

|

g. Transferor/seller’s share of total payment (multiply line e by line f) |

|

|

|

g |

|

|

|

|

● |

|||||||

|

h. Enter applicable rate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1) 2.5% of total payments, or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2) 6.5% of estimated capital gain $__________________ |

|

|

|

h |

|

% |

|

|

||||||||

|

i. WV Income Tax withheld (multiply line g or amount of estimated capital gain by line h) |

|

|

|

|

|

|

|

|

|

|||||||

|

(If partial exemption granted, enter amount stated on Form WV/NRCE) |

|

|

|

i |

|

|

|

|

● |

|||||||

copy c – For issuer

Document Specifics

| Fact | Detail |

|---|---|

| 1. Purpose | The form is used for the withholding of West Virginia income tax on the sale of real property by nonresidents. |

| 2. Required Filers | Nonresident individuals and entities selling real property in West Virginia must file the WV/NRSR form. |

| 3. Filing Requirement for Joint Returns | A separate form is needed for each transferor/seller unless a husband and wife are filing a joint WV income tax return. |

| 4. When to File | The form must be completed at the time of sale closing unless the transaction is exempt from the income tax withholding requirement. |

| 5. Computation of Tax to Withhold | Tax is calculated based on the sale price minus any deductions, with rates of 2.5% of total payments or 6.5% of estimated capital gain. |

| 6. Submission Process | File Copy A of the form with the WV State Tax Department, provide Copy B to the transferor/seller, and retain Copy C for records. |

| 7. Governing Law | The form and process are governed by West Virginia state law, specifically for tax duties related to nonresident transactions of real property. |

Guide to Using Wv Nrsr

Completing the WV/NRSR form is an essential step for nonresident sellers of real estate in West Virginia. This process ensures the correct amount of income tax is withheld from the sale of the property. Proper completion and timely submission of this form prevent any potential issues with the West Virginia State Tax Department. Follow these detailed steps to accurately fill out the form.

- Property account ID Number: Insert the property account ID number as listed by the county assessor. If the property comprises multiple parcels, include all account numbers.

- Date of transfer: Enter the date the property was transferred to the new owner. Use the format MM DD YYYY.

- Check if under the installment method: Mark the box if the transferor/seller is reporting the gain under the installment sale method.

- Transferor/Seller’s Identification number: Choose the appropriate identification number type - SSN, FEIN, or ITIN and provide the number.

- Spouse’s SSN Number: If applicable, enter the spouse's Social Security Number (only when filing a joint return).

- Transferor/Seller’s name: Write the name of the transferor/seller. If the property is owned by more than one person (and they are not husband and wife filing jointly), separate forms are required for each.

- Transferor/Seller’s address: Provide the street address, including City, State, and Zip Code of the transferor/seller. Do not enter the property's address being transferred here.

- Transferor/Seller is: Mark the appropriate box that identifies the transferor/seller’s status (e.g., Individual, Corporation, Trust).

- Computation of total payment and tax to be withheld:

- a. Enter the total sales price paid to the transferor

- b. Deduct selling expenses

- c. Deduct debts secured by mortgages or other liens on the property

- d. Calculate net proceeds

- e. Note the total payments made to the transferor

- f. Enter the transferor/seller’s ownership percentage

- g. Calculate the transferor/seller’s share of the total payment

- h. Enter the applicable rate for tax computation

- i. Calculate the WV Income Tax withheld

- At the bottom of the form, the transferor/seller or an authorized representative must sign and date, certifying the accuracy of the information provided.

Once the form is completed, it should be attached to a check or money order for the total amount of tax due. This payment should be made to the West Virginia State Tax Department. Mail the form and payment to the specified address on the form. Remember, timely filing is crucial to comply with West Virginia state requirements and avoid any potential penalties. The form serves as a critical document to ensure that nonresident sellers meet their tax obligations associated with the sale of real property in West Virginia.

Essential Points on Wv Nrsr

What is the WV/NRS™ form and why is it required?

The WV/NRSR form is a document required by the West Virginia State Tax Department. Its primary purpose is to ensure the collection of income tax from nonresident individuals or entities when they sell real property located within West Virginia. This form calculates the amount of income tax that needs to be withheld at the time of sale or transfer and facilitates its collection, ensuring nonresident sellers meet their tax obligations.

Who needs to file the WV/NRSR form?

Nonresident individuals or entities transferring an interest in real property located within West Virginia must complete the WV/NRSR form, unless the transaction is exempt from income tax withholding requirements. This includes individuals who do not reside in West Virginia, as well as entities not formed under the laws of West Virginia or not registered to do business in the state. For transactions involving multiple nonresident sellers, a separate form is required for each seller.

When should the WV/NRSR form be submitted?

The form must be submitted to the West Virginia State Tax Department within 30 days of the date the amounts were withheld, coinciding with the closing of the property sale. Timely submission ensures compliance with state tax obligations and helps avoid any potential penalties.

What information is required on the WV/NRSR form?

The form requests detailed information about the property sale, including the property account ID number, date of transfer, transferor/seller's identification number(s), and a comprehensive computation of the total payment and tax to be withheld. It also includes specifics such as the total sales price, less selling expenses and debts secured by the property, and calculates the withholding tax based on the seller’s ownership percentage and applicable tax rate.

How is the tax withholding amount calculated on the form?

Tax withholding is calculated by first determining the net proceeds from the sale, which involves deducting any mortgages, liens, selling expenses, and other costs from the total sales price. The transferor/seller's share of the total payment is then multiplied by the applicable tax rate, which can be either 2.5% of total payments or 6.5% of the estimated capital gain. The resulting amount is the income tax required to be withheld.

What happens if there are multiple owners of the property?

If the property is owned by multiple parties, each owner's share must be individually determined, and the tax withholding calculated accordingly. Each nonresident owner must file a separate WV/NRSR form, reflecting their share of the ownership and the related income tax withholding.

How can I claim the income tax that has been withheld?

The income tax withheld can be claimed by submitting a copy of the WV/NRSR form (Copy B) with the appropriate West Virginia income tax return for the year in which the transfer occurred. The type of income tax return required depends on the seller's status (individual, corporation, partnership, trust, etc.). Failure to include this form with the tax return may result in the disallowance of the withholding tax credit.

Are there any exemptions to the withholding requirement?

Yes, certain transactions may be exempt from the income tax withholding requirement. If the West Virginia State Tax Commissioner issues a Certificate of Partial Exemption, the tax withholding calculation section of the form should be skipped, and only the amount stated on the certificate should be withheld. It’s important to review the specific criteria for exemptions and consult with the West Virginia State Tax Department or a tax professional if you believe your transaction qualifies for one.

Common mistakes

Filling out the WV/NRSR form, which pertains to the Return of Income Tax Withholding for Nonresident Sale of Real Property in West Virginia, can be complex. Obstacles often arise due to the form's detailed requirements and specificity. Here are nine common mistakes individuals make when completing this form:

- Improper identification of the Property Account ID Number is a frequent error. This number is crucial as it uniquely identifies the property in question, ensuring the correct processing of the form.

- Another common mistake is providing an incorrect Date of Transfer. The date must reflect the effective date of the deed, which is either the date of the last acknowledgment or the date stated in the deed itself.

- Failure to check the box when the transferor/seller is reporting gain under the installment method can lead to inaccuracies in tax calculations.

- Mixing up identification numbers, such as the Transferor/Seller’s Identification number, and if applicable, the Spouse’s SSN Number, can cause significant processing delays.

- Not specifying the type of transferor/seller in section 7 (for example, individual, corporation, trust, etc.) may result in the form being returned for correction.

- Calculating the total payment and tax to be withheld without properly accounting for selling expenses, debts secured by mortgages, or other pertinent deductions can inflate the tax liability.

- Incorrectly estimating the transferor/seller’s ownership percentage can impact the computation of the transferor/seller’s share of total payment, thereby affecting the tax withheld.

- Misapplying the applicable tax rate when determining the WV income tax withheld can either cause an overpayment or underpayment of taxes.

- Failure to properly sign and date the form, or if prepared by someone other than the transferor/seller, neglecting to ensure that the preparer’s declaration is based on all information to which the preparer has any knowledge.

To avoid these errors, individuals should thoroughly review the form and accompanying instructions before submission. Details such as accurately reporting the total sales price, deducting all entitled expenses, and correctly calculating the net proceeds are crucial for accurate tax withholding. Additionally, consulting with a tax professional or the West Virginia State Tax Department for clarification can help ensure the form is completed accurately.

In summary, attention to detail and a thorough understanding of the specific requirements for the WV/NRSR form can prevent these common mistakes. By avoiding these pitfalls, individuals can ensure a smoother process in the withholding of income tax for the nonresident sale of real property in West Virginia.

Documents used along the form

When dealing with the sale of real property by nonresidents in West Virginia, the WV/NRSR form serves as a critical document for reporting and withholding income tax. Alongside this form, several other documents often play pivotal roles throughout the real estate transaction process, ensuring compliance with state tax laws and facilitating smooth property transitions. Highlighting these documents provides a more comprehensive understanding of the administrative responsibilities surrounding such sales.

- Closing Disclosure: This form provides a detailed account of the real estate transaction, including the sale price, loan information, closing costs, and other financial details. It's crucial for calculating the net proceeds from the sale, which in turn aids in completing the WV/NRSR form.

- Form WV/NRCE (Nonresident Withholding Tax Exemption Certificate): If certain conditions are met that exempt the seller from nonresident withholding tax, this form is used to apply for an exemption. When granted, it modifies the withholding requirements on the WV/NRSR form.

- Deed of Sale: This legal document officially transfers ownership of the property from the seller to the buyer. It provides essential information such as property description and the parties involved, necessary for the WV/NRSR form's completion.

- IRS Form 8288 (U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests): For nonresident aliens selling U.S. real property, this IRS form is used to report and remit the required federal withholding. While it's a federal form, understanding the interplay between federal and state tax obligations is critical.

- Power of Attorney: In transactions where the nonresident seller cannot be present, a Power of Attorney may be granted to an individual to sign documents, such as the WV/NRSR form, on behalf of the seller. This document ensures legal representation and the authority to conduct transactions.

Understanding and preparing these forms and documents are fundamental steps to ensuring legal compliance and successful real estate transactions involving nonresident sellers in West Virginia. The synergy between these documents and the WV/NRSR form helps streamline the process, from the sale's initiation to the final tax reporting and withholding.

Similar forms

The WV/NRSR Return of Income Tax Withholding for Nonresident Sale of Real Property shares similarities with the IRS Form 8288, U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests. Both forms are used in the context of real estate transactions and are designed to collect income tax at the time of the property sale. The WV/NRSR form focuses on nonresident sellers of real property located within West Virginia, whereas Form 8288 applies to foreign persons disposing of U.S. real property interests. Each form serves to ensure compliance with state and federal tax laws, respectively, by requiring the withholding of tax on the sale of real property to cover potential tax liabilities of the sellers.

Similarly, the California Form 593, Real Estate Withholding Statement, has a common purpose with the WV/NRSR form as it pertains to real estate transactions. The California form is used for withholding tax on the sale of real property within the state of California, focusing specifically on ensuring that nonresident sellers meet their state tax obligations. Like the WV/NRSR form, Form 593 requires information on the sale price, the seller, and the amount of tax withheld and aims to capture tax due from the sale at the time of the transaction.

The New York State Form IT-2663, Nonresident Real Property Estimated Income Tax Payment Form, is another document with a function similar to the WV/NRSR form. It is designed for nonresident individuals selling real property located in New York State, requiring the seller to calculate and pay estimated income tax on the capital gains from the sale. Both forms share the goal of capturing tax revenue at the source to ensure that nonresident sellers fulfill their tax obligations related to the sale of property.

The Colorado DR 1083, Withholding Tax Return for Dispositions by Nonresidents of Colorado Real Property, parallels the WV/NRSR form by focusing on the collection of state income tax from nonresidents selling real property within the jurisdiction. Each of these forms ensures compliance with state tax laws by mandating the withholding of income tax directly from the transaction proceeds, thus securing tax collection from nonresidents who may not otherwise file state tax returns.

Form 1099-S, Proceeds from Real Estate Transactions, though a federal form issued by the IRS, bears resemblance to the WV/NRSR form in that it is used in the reporting of real estate transactions. Form 1099-S is often required when a real estate sale triggers tax reporting obligations. While the 1099-S focuses more broadly on reporting to the IRS and to the seller for their tax records, it intersects with the purpose of the WV/NRSR form by ensuring proper documentation and taxation of real estate transactions.

The Oregon Form OR-18, Withholding Tax Statement for Transfer or Conveyance of Real Property Interest, shares similarities with the WV/NRSR form as it is designed to facilitate the withholding and remittance of state taxes on the sale of real property by nonresidents. Both forms play a crucial role in the tax administration process by requiring withholdings to secure tax payments upfront, mitigating the risk of non-compliance by nonresident sellers.

The Pennsylvania REV-183, Realty Transfer Tax Statement of Value, although primarily a document for calculating transfer taxes rather than income taxes, shares a conceptual similarity with the WV/NRSR form in the context of real estate transactions. Both documents are integral to the transfer process, ensuring that appropriate taxes related to the sale of real property are assessed and collected in a timely manner.

Maryland's Form MW506AE, Application for Certificate of Full or Partial Exemption for the Sale of Real Property by a Nonresident, is another document with functional similarities to the WV/NRSR form. This form is part of Maryland's approach to managing tax obligations of nonresident sellers, allowing for the determination of exemptions in certain cases. Both the WV/NRSR form and the MW506AE facilitate a mechanism to ensure that nonresident sellers meet their tax responsibilities in relation to the sale of real property.

The Florida Nonresident Withholding Form, though specific to Florida and not applicable in all circumstances, serves a similar purpose to the WV/NRSR by addressing tax withholding on transactions involving nonresident sellers of real estate. The focus across both forms on nonresident sellers underscores a common challenge for state tax authorities in capturing tax revenue from real estate transactions involving parties who do not reside within the state.

Finally, the Arizona Form 8213R, Nonresident Withholding Real Property Sale, parallels the WV/NRSR form in its aim to collect state taxes from nonresident sellers at the time of a real estate transaction. Both forms represent state-level efforts to ensure that nonresidents contribute their fair share of taxes on the gains from the sale of property, emphasizing the importance of withholding mechanisms as tools for tax compliance and enforcement.

Dos and Don'ts

When filling out the WV/NRSR form for nonresident sale of real property in West Virginia, it is important to follow several do's and don'ts to ensure the process is smooth and error-free. This guidance aims to assist with accurate form completion and compliance with West Virginia State Tax Department requirements.

Do's:- Review the entire form before starting. Understand each section to ensure all relevant fields are completed correctly.

- Use the correct Property Account ID Number. This number is crucial for identifying the property being transferred.

- Clearly mark the date of transfer. Ensure the MM DD YYYY format is followed as per the form's instructions.

- Check the appropriate box for the transferor/seller's status. Whether an individual, corporation, or another entity, selecting the correct classification is vital.

- Accurately calculate the total payment and tax to be withheld. Double-check calculations for net proceeds, the transferor/seller’s share of total payment, and applicable tax rates.

- Sign and date the form where required. A form without a signature may not be processed.

- Keep a copy for records. Ensuring you have a record of the submitted form is important for future reference.

- Submit the form and payment on time. Adhere to the 30-day submission rule to avoid penalties.

- Don’t leave any required fields blank. Incomplete forms may result in processing delays or rejection.

- Don’t guess on figures or information. Use exact numbers and double-check all entries for accuracy.

- Don’t use the street address of the property in place of the Property Account ID Number. These are distinct identifiers, and using the wrong one can lead to misprocessing.

- Don’t ignore the separate form requirement for multiple transferors/sellers. If there is more than one transferor/seller, a separate form is required for each, unless filing a joint return as a married couple.

- Don’t overlook the installment method box if applicable. If reporting gain under the installment method, make sure to check the relevant box.

- Don’t underestimate the importance of the form’s instructions. The detailed instructions are there to help navigate the complexities of the form.

- Don’t send the form to the wrong address. Confirm the mailing address is correct as per the form's instructions.

- Don’t hesitate to seek help if uncertain. Misinterpretation can lead to errors, so requesting assistance from a professional or the tax department for unclear areas is advisable.

Following these guidelines when completing the WV/NRSR form will help ensure the process is completed efficiently and accurately, fulfilling your tax obligations without unnecessary complications.

Misconceptions

When navigating the intricacies of the WV/NRSR form, which handles income tax withholding for nonresident sales of real property in West Virginia, it's easy to stumble over misconceptions. Understanding the realities can help simplify the process, ensuring compliance and peace of mind. Below are ten common misunderstandings about the WV/NRSR form and the truths behind them:

- Only applicable for sales exceeding a certain amount: The requirement to complete the WV/NRSR form does not depend on the sales price or value of the real property. Any sale of real property located in West Virginia by a nonresident individual or entity is subject to this form, irrespective of the sale price.

- It’s a one-size-fits-all form: Each nonresident seller involved in the transaction must complete a separate WV/NRSR form. However, an exception is made for married couples filing a joint return, who can report on a single form.

- Personal residence sales are exempt: The status of the property as a personal residence does not automatically exempt the sale from WV/NRSR filing requirements. Nonresident sellers must report the transaction unless another specific exemption applies.

- Filing is optional for sellers without a taxable gain: Even if the sale does not result in a taxable gain for the nonresident, the filing of the WV/NRSR and proper income tax withholdings are required by law, ensuring compliance with West Virginia state tax regulations.

- Withholding rates are negotiable: The withholding rates are fixed by law at either 2.5% of the total payments or 6.5% of the estimated gain and are not subject to negotiation or adjustment by either party in the transaction.

- Non-US citizens cannot file this form: Nonresident alien individuals and foreign entities must also comply with the WV/NRSR filing and withholding requirements if they sell real property located in West Virginia.

- Income tax withholding applies only to profit from the sale: The withholding is calculated on either the total payment made to the transferor/seller or on the estimated capital gain, not solely on the actual profit or gain realized from the sale.

- You can submit the form electronically: As of the last information available, the form and accompanying tax payment must be submitted by mail to the West Virginia State Tax Department, not electronically.

- Extension for filing is automatically granted: There are strict deadlines for filing the WV/NRSR form, usually within 30 days after the date the amounts were withheld. Requests for extensions are not automatically granted and must comply with specific procedural requirements.

- The seller's Social Security Number is enough for identification: While a Social Security Number is required for individual sellers, other identifying numbers, such as the FEIN for corporations or ITIN for foreign entities, are also necessary depending on the nature of the seller.

Correctly understanding and applying the requirements of the WV/NRSR form is crucial for nonresident sellers in West Virginia. This ensures a smooth transaction process and adherence to state tax obligations, avoiding potential penalties or complications. Consultation with a tax professional is advisable to navigate the specifics of your situation confidently.

Key takeaways

Filling out and using the West Virginia Nonresident Seller of Real Property (WV/NRSR) form involves several critical steps and considerations for ensuring that income tax withholding for the sale of real property by nonresidents is accurately reported and paid. The following key takeaways provide guidance through this process:

- The purpose of the WV/NRSR form is to facilitate the collection of income tax due from nonresident individuals or entities selling real property located in West Virginia.

- Nonresident individuals or entities engaged in the transfer of real property in West Columbia must file the form, unless the transaction is exempt from the income tax withholding requirement.

- If the property sale involves multiple nonresident transferor/sellers, a separate WV/NRSR form must be completed for each person, except in cases where a married couple is filing a joint return.

- The form requires detailed information about the sale, including the property account ID number, date of transfer, and whether the gain is reported under the installment method.

- Sellers must indicate their type, such as individual, corporation, trust, or another entity, by checking the appropriate box on the form.

- Calculation of the tax to be withheld is based on the net proceeds from the sale, the seller's ownership percentage, and applicable tax rates, either 2.5% of total payments or 6.5% of estimated capital gain, depending on the situation.

- If an installment sale is reported, sellers should note this on the form, as this may affect how the gain is recognized and taxed over time.

- Payment of the withholding tax must accompany the submission of the WV/NRSR form to the West Virginia State Tax Department within 30 days following the date the amounts were withheld.

- Transferor/sellers should keep a copy of the form (Copy B) for their records, as it is essential for claiming the income tax withheld when filing their income tax return.

- Nonresident sellers need to file a West Virginia income tax return for the year the transfer of property occurred, attaching a copy of the WV/NRSR to claim the withholdings.

This structured approach ensures that nonresident sellers comply with West Virginia's tax laws and avoid potential issues with underpayment or nonpayment of taxes on the sale of real property.

Popular PDF Forms

West Virginia Board of Accountancy - Fulfill your professional responsibility by renewing your CPA license on time and avoiding any unauthorized practice risks.

Wv Court Forms - This form is used exclusively for appealing a final judgment from a Circuit Court in West Virginia to the Supreme Court of Appeals.

College Online Application - Concretizes the academic achievements necessary for scholarship eligibility, reinforcing the value of high academic standards.