Fill Out a Valid Wv 8379 Form

The WV 8379 form, developed by the West Virginia State Tax Department, serves an essential purpose for married couples who file their tax returns jointly but find themselves in situations where their tax refund is intercepted due to the debts of one spouse, such as unpaid child support or tax obligations. Deemed the "Injured Spouse Allocation," this document is a strategic tool that allows for the equitable distribution of a tax refund between spouses, ensuring that the party not responsible for the debt can reclaim their share of the refund. Comprehensive in its approach, the form demands detailed information about both spouses and their financial contributions, including each spouse's income, any additions or subtractions to their federal adjusted gross income as reported on West Virginia tax returns, and specifics about exemptions, tax withholding, estimated tax payments, and applicable credits. The form’s meticulous design ensures a fair allocation of joint income and individual tax liabilities, with clear instructions for attaching tax statements and handling the peculiarities of non-resident or part-year tax returns. For couples navigating the complexities of tax obligations amidst individual financial liabilities, completing the WV 8379 form is a crucial step towards financial fairness and clarity.

Sample - Wv 8379 Form

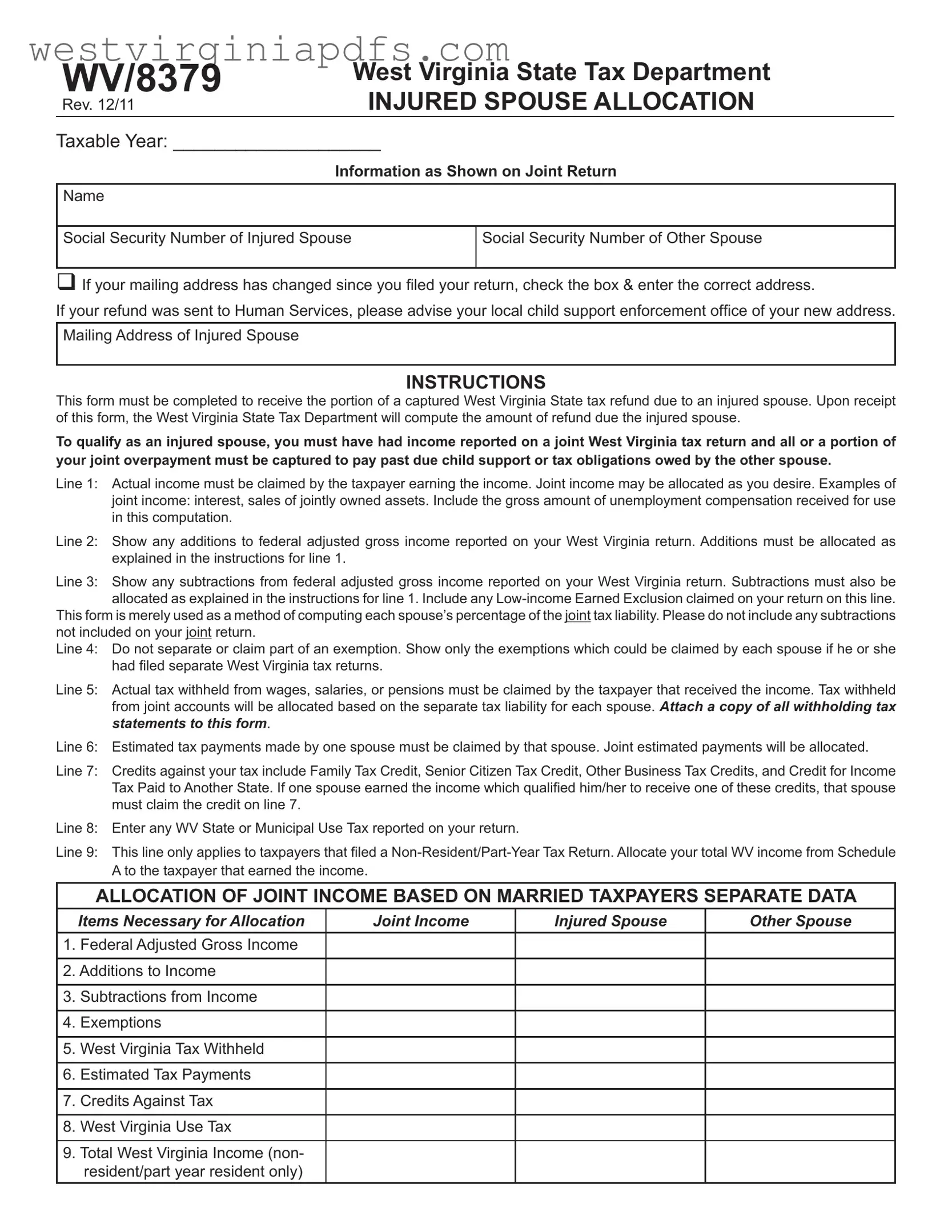

WV/8379 |

West Virginia State Tax Department |

|

INJURED SPOUSE ALLOCATION |

||

Rev. 12/11 |

Taxable Year: ____________________

Information as Shown on Joint Return

Name

Social Security Number of Injured Spouse

Social Security Number of Other Spouse

If your mailing address has changed since you iled your return, check the box & enter the correct address.

If your refund was sent to Human Services, please advise your local child support enforcement ofice of your new address.

Mailing Address of Injured Spouse

INSTRUCTIONS

This form must be completed to receive the portion of a captured West Virginia State tax refund due to an injured spouse. Upon receipt of this form, the West Virginia State Tax Department will compute the amount of refund due the injured spouse.

To qualify as an injured spouse, you must have had income reported on a joint West Virginia tax return and all or a portion of your joint overpayment must be captured to pay past due child support or tax obligations owed by the other spouse.

Line 1: Actual income must be claimed by the taxpayer earning the income. Joint income may be allocated as you desire. Examples of joint income: interest, sales of jointly owned assets. Include the gross amount of unemployment compensation received for use

in this computation.

Line 2: Show any additions to federal adjusted gross income reported on your West Virginia return. Additions must be allocated as explained in the instructions for line 1.

Line 3: Show any subtractions from federal adjusted gross income reported on your West Virginia return. Subtractions must also be allocated as explained in the instructions for line 1. Include any

This form is merely used as a method of computing each spouse’s percentage of the joint tax liability. Please do not include any subtractions not included on your joint return.

Line 4: Do not separate or claim part of an exemption. Show only the exemptions which could be claimed by each spouse if he or she had iled separate West Virginia tax returns.

Line 5: Actual tax withheld from wages, salaries, or pensions must be claimed by the taxpayer that received the income. Tax withheld

from joint accounts will be allocated based on the separate tax liability for each spouse. Attach a copy of all withholding tax statements to this form.

Line 6: Estimated tax payments made by one spouse must be claimed by that spouse. Joint estimated payments will be allocated.

Line 7: Credits against your tax include Family Tax Credit, Senior Citizen Tax Credit, Other Business Tax Credits, and Credit for Income Tax Paid to Another State. If one spouse earned the income which qualiied him/her to receive one of these credits, that spouse

must claim the credit on line 7.

Line 8: Enter any WV State or Municipal Use Tax reported on your return.

Line 9: This line only applies to taxpayers that iled a

A to the taxpayer that earned the income.

ALLOCATION OF JOINT INCOME BASED ON MARRIED TAXPAYERS SEPARATE DATA

|

Items Necessary for Allocation |

Joint Income |

Injured Spouse |

Other Spouse |

|

|

|

|

|

1. |

Federal Adjusted Gross Income |

|

|

|

|

|

|

|

|

2. Additions to Income |

|

|

|

|

|

|

|

|

|

3. |

Subtractions from Income |

|

|

|

|

|

|

|

|

4. |

Exemptions |

|

|

|

|

|

|

|

|

5. |

West Virginia Tax Withheld |

|

|

|

|

|

|

|

|

6. |

Estimated Tax Payments |

|

|

|

|

|

|

|

|

7. |

Credits Against Tax |

|

|

|

|

|

|

|

|

8. |

West Virginia Use Tax |

|

|

|

|

|

|

|

|

9. Total West Virginia Income (non- |

|

|

|

|

|

resident/part year resident only) |

|

|

|

|

|

|

|

|

Document Specifics

| Fact Number | Fact Detail |

|---|---|

| 1 | The WV/8379 form is officially titled "Injured Spouse Allocation" and it is specific to the West Virginia State Tax Department. |

| 2 | This form is dedicated to helping an injured spouse reclaim a portion of their West Virginia State tax refund that was captured for the other spouse's past due child support, tax obligations, or other debts. |

| 3 | Eligibility for filling out the WV/8379 form requires the injured spouse to have reported income on a joint West Virginia tax return and part of their joint overpayment must have been captured for debts owed by the other spouse. |

| 4 | The form allows for the allocation of joint income, additions and subtractions to income, exemptions, and tax credits between the injured and the other spouse to fairly distribute the tax liability and refund. |

| 5 | Documentation, such as withholding tax statements, is required to be attached to the form for claims on tax withheld from wages, salaries, pensions, and estimated tax payments. |

| 6 | The governance for the WV/8379 form, including its requirements and the process of allocation, is under the jurisdiction of West Virginia state law. |

Guide to Using Wv 8379

Filling out the WV 8379 form is a necessary step for individuals looking to claim their share of a tax refund when the other spouse's debt obligations lead to the state capturing the joint tax refund. It's essential for recovering what an injured spouse is rightfully due. The process involves reporting incomes, deductions, credits, and taxes paid individually by each spouse, despite having filed a joint tax return. Understanding each section of the form ensures accurate representation of both spouses' financial contributions and liabilities, setting the stage for a fair allocation of the refund.

- Begin with the Taxable Year at the top of the form, entering the year for which you are claiming injured spouse relief.

- Under Information as Shown on Joint Return, fill in the full name and Social Security Number (SSN) for both the injured spouse (the one not responsible for the debt that led to the refund being captured) and the other spouse.

- If your mailing address has changed since filing your return, check the box next to that line and write your current address.

- Advanced to ALLOCATION OF JOINT INCOME BASED ON MARRIED TAXPAYERS SEPARATE DATA. Beginning with Line 1, enter the Federal Adjusted Gross Income (FAGI) and allocate it between the injured spouse and the other spouse as accurately as possible based on individual earnings.

- On Line 2, list any additions to income you reported on your West Virginia return and divide them between spouses as per instructions.

- Line 3 requires you to report any subtractions from your FAGI that you included on your return. Allocate these amounts between spouses.

- For Line 4, indicate the exemptions that each spouse could claim if they filed separate West Virginia tax returns.

- Fill in Line 5 with the actual amount of West Virginia tax withheld from each spouse's wages, salaries, or pensions. Attach copies of all withholding tax statements.

- On Line 6, note the estimated tax payments made by each spouse. Joint estimated payments must be allocated between the two.

- Line 7 is for credits against tax. If one spouse qualifies for credits like the Family Tax Credit or Senior Citizen Tax Credit based on their income, they should claim the credit here.

- Enter any West Virginia State or Municipal Use Tax reported on your joint return in Line 8.

- Line 9 is specifically for taxpayers who filed a Non-Resident/Part-Year Tax Return. Allocate your total West Virginia income from Schedule A based on who earned the income.

- Review the entire form to ensure all information is accurate and complete. Attach any required documentation, such as withholding tax statements, before submitting the form to the West Virginia State Tax Department.

After you've filled out the form thoroughly, it's time to submit it to the West Virginia State Tax Department. This is a critical step in ensuring that you receive the portion of the tax refund you're entitled to, independent of any debt obligations solely belonging to your spouse. It can take some time for the department to process your claim, so patience is essential. Once processed, you will be notified of the outcome and can expect to receive any allocated refund due to you.

Essential Points on Wv 8379

What is the WV 8379 form used for?

The WV 8379 form, officially named the Injured Spouse Allocation form, is utilized by individuals to claim their share of a West Virginia state tax refund. This situation arises when a joint tax refund is intercepted to cover the past due child support, tax obligations, or other debts owed by the other spouse. By completing this form, an injured spouse can request to receive their portion of the tax refund that they are rightfully entitled to, based on the income and taxes they individually contributed to the joint tax return.

Who qualifies as an ‘injured spouse’?

To qualify as an injured spouse, an individual must meet specific criteria. Firstly, the person must have reported income on a joint West Virginia tax return. Additionally, a part of or the entire joint tax overpayment must have been captured to offset debts such as past due child support or tax obligations, which are solely attributable to the other spouse. Essentially, an injured spouse is someone whose share of a joint refund has been or is at risk of being used to cover the other spouse's liabilities.

How is joint income allocated on the WV 8379 form?

Joint income is allocated on the WV 8379 form based on each spouse’s contribution and the nature of the income. Line 1 of the form specifically mentions that actual income should be claimed by the spouse who earned it, and joint income can be allocated as desired. Types of joint income can include interest from joint accounts, proceeds from the sale of jointly owned properties, and unemployment compensation. Each party must allocate additions to and subtractions from their federal adjusted gross income on the form to accurately compute each spouse's share of the tax liability.

What documents need to be attached to the WV 8379 form?

When filing the WV 8379 form, it's essential to attach all withholding tax statements to the form. This documentation is crucial as it supports the actual tax withheld from the wages, salaries, or pensions reported on the form, which must be claimed by the spouse who received the income. If any credits against tax are claimed, the corresponding proof must also accompany the claim to verify the eligibility and correctness of the claimed amounts.

Can estimated tax payments and tax credits be allocated between spouses?

Yes, estimated tax payments and tax credits can indeed be allocated between spouses on the WV 8379 form. Tax payments made by one spouse should be claimed by that spouse on line 6 of the form. If the payments were made jointly, they would be allocated based on the separate tax liabilities of each spouse. Similarly, credits against the tax, such as the Family Tax Credit or Senior Citizen Tax Credit, must be claimed by the spouse who earned the income qualifying for the credit. This allocation ensures that each spouse’s contribution to the tax liability and qualifying credits is accurately reflected.

Common mistakes

The intricacies of filling out tax forms can be daunting, especially when it comes to forms designed to address specific circumstances, like the WV 8379 form for injured spouses in West Virginia. Completing this form correctly is crucial for those seeking to claim their rightful portion of a tax refund that might otherwise be used to offset their partner's debts, such as overdue child support or tax obligations. Here are eight common mistakes to avoid:

Not verifying the accuracy of personal information: It's essential to double-check that all personal details, especially your social security number and mailing address, are accurate and current. If your address has changed and you don't mark the appropriate box and update your address on the form, you may encounter delays.

Incorrectly allocating income: The division of actual income and joint income between spouses is a crucial step that's often mishandled. Each spouse must claim the income they earned individually, and joint income must be allocated as decided upon, which requires careful consideration and accurate reporting.

Overlooking additions and subtractions to income: Additions and subtractions to the federal adjusted gross income need to be reported with the same care as the initial income figures. These adjustments must be allocated accurately according to the instructions to avoid miscalculations in the refund due.

Failing to properly attach withholding tax statements: Neglecting to attach all necessary withholding tax statements for wages, salaries, or pensions can result in processing delays or incorrect allocations of withheld taxes between spouses.

Misallocating estimated tax payments and withholding: It's a common error to incorrectly claim estimated tax payments or tax withheld from joint accounts. Those must be allocated based on who made the payments or whose income was subject to withholding.

Incorrectly claiming tax credits: Only the spouse who earned the income qualifying for tax credits such as the Family Tax Credit or Senior Citizen Tax Credit should claim them. Misattributing these credits can affect the refund amount.

Omitting state or municipal use tax: Forgetting to enter any WV State or Municipal Use Tax reported on your return can throw off the accuracy of the form, leading to discrepancies in your refund calculation.

Allocation errors for non-residents or part-year residents: Non-residents or part-year residents must carefully allocate their total WV income on Schedule A to the correct taxpayer. Incorrect allocations can lead to errors in how much refund the injured spouse is entitled to.

When filling out the WV 8379 form, due diligence, accuracy, and thoroughness are your best allies. Steering clear of these common mistakes not only helps ensure that the process goes smoothly but also maximizes the likelihood of receiving the correct portion of the tax refund. Remember, when in doubt, consulting a tax professional can provide clarity and guidance tailored to your specific situation.

Documents used along the form

When dealing with the complexities of family financial matters, particularly in situations requiring the submission of WV 8379 form for the injured spouse allocation, being prepared with the necessary documents is crucial. This form is essential for spouses who, though they filed jointly, are not responsible for debts or tax obligations that have led to the state capturing their tax refund. However, the WV 8379 form is just a part of a suite of documents that may be needed to navigate the legal and tax implications of such situations effectively. Below are other documents often used alongside the WV 8379 form:

- IRS Form 8379: This is the federal counterpart to the WV 8379, used for allocating a joint tax refund when it's been offset to cover the other spouse’s past-due obligations like federal taxes, child or spousal support, or federal debts such as student loans.

- State Tax Return: The most recent state tax return filed jointly. It is crucial as it provides the base figures used in the allocation process.

- Proof of Withholding and Estimated Tax Payments: W-2s, 1099s, and records of estimated tax payments are needed to substantiate the amounts entered on the WV 8379 form, specifically in the sections asking for tax withheld and estimated payments made.

- Statement of Income: Documents that verify the income of both spouses, which could include pay stubs, employer statements, or 1099-MISC forms for independent contractors. This supports the allocation of income between the spouses.

- Notice of Offset: The official notice received when a tax refund is applied to a past-due obligation, explaining why the offset was made. This notice helps in clarifying the reason for filing the WV 8379 form.

- Debt Documentation: Documents that prove the existence and status of the debt that led to the offset, such as statements of account for child support arrears or notification of non-payment of taxes.

- Credit for Income Tax Paid to Another State: If applicable, documentation that supports any claim for tax credits due to taxes paid in another state, which affects how much of the refund may be owed to the injured spouse.

- Schedule of Joint Income Allocation: A detailed breakdown of how each portion of joint income, deductions, and credits are allocated between spouses. While some of these details are part of the WV 8379, a more comprehensive schedule might be needed for complex cases.

Together, these documents equip taxpayers with the means to articulate and substantiate their claim under the injured spouse allocation, ensuring that each party receives their fair share of any tax refund due. It’s advisable to gather these documents early in the process to facilitate a smoother submission and a faster resolution. Consulting with a tax professional can also provide valuable guidance through what can be a complex and stressful process.

Similar forms

The Form 8379, Injured Spouse Allocation, shares similarities with the IRS Form 8857, Request for Innocent Spouse Relief. Both forms are designed to protect the tax interests of one spouse from the debts or liabilities of the other. While the WV 8379 form specifically deals with obtaining a portion of a state tax refund that was intercepted due to the other spouse's debts, such as back taxes or child support, Form 8857 requests relief from joint tax liability for federal taxes. Both seek to allocate financial responsibility based on the individual circumstances of each spouse, but they do so in the context of different types of tax obligations and jurisdictions.

The IRS Form 1040X, Amended U.S. Individual Income Tax Return, bears a resemblance to the WV 8379 in that it is used to correct or update a previously filed tax return, potentially affecting allocations of payments or refunds. While the 8379 form is specifically for reallocating a refund between spouses due to a garnishment or debt of one spouse, the 1040X can be used by anyone needing to amend their tax return for a variety of reasons, including changes in filing status, income, deductions, or credits. Both forms involve recalculating taxes owed or refunds due, but with different objectives and outcomes.

Form 8379 parallels the functionality of the IRS Form 8888, Allocation of Refund (Including Savings Bond Purchases), in the aspect of directing the distribution of refunds. Form 8888 enables taxpayers to allocate their federal tax refund among different accounts or to purchase savings bonds, thereby exerting control over where their refund goes. Similarly, WV 8379 allows the injured spouse to reclaim their portion of a joint tax refund that would otherwise be offset by the other spouse's debts. Both forms grant individuals power over the allocation of funds, but they serve different purposes within the scope of tax refunds and liabilities.

Another counterpart, albeit focused on a different aspect of tax penalty relief, is the IRS Form 843, Claim for Refund and Request for Abatement. This form is used to request a refund or ask for an abatement of certain taxes, penalties, interest, fees, and additions to tax. Like the WV 8379, Form 843 is employed when a taxpayer believes they have been incorrectly or unfairly charged. While Form 843 is broader in its application, covering a range of taxes and charges, WV 8379 is specifically designed to deal with the allocation of a state tax refund between spouses when one is an "injured" party.

The Comparison of Household Employment Taxes (Schedule H) for completing IRS Form 1040 closely aligns with the principle behind WV 8379 in terms of allocating financial responsibilities. Schedule H is utilized for reporting taxes for household employees on the taxpayer's federal tax return. Like WV 8379, it involves determining the correct allocation of taxes (in this case, employment taxes for household employees), but it operates in the domain of employer responsibilities rather than between spouses.

Lastly, Form 9465, Installment Agreement Request, shares the notion of addressing outstanding tax liabilities in a manner tailored to the taxpayer's situation, much like the WV 8379. While Form 9465 is for taxpayers who cannot pay their full tax liability immediately and wish to make monthly installment payments, WV 8379 addresses the allocation of a refund due to such liabilities. Both forms provide mechanisms for dealing with tax debts, albeit from different angles—Form 9465 focuses on the payment plan for liabilities, and WV 8379 on the protection and allocation of refunds.

Dos and Don'ts

When filling out the WV 8379 form for the West Virginia State Tax Department, individuals seeking injured spouse relief should carefully navigate the process. Here are 10 essential do's and don'ts to guide you through the completion of this important document:

- Do ensure that the injured spouse's name and Social Security Number are filled in correctly to prevent any processing delays.

- Do check the box if your mailing address has changed since you filed your return. It’s crucial for receiving any correspondence or the refund due without unnecessary delay.

- Do accurately allocate joint income, such as interest or sales from jointly owned assets, between the injured spouse and the other spouse, reflecting the individual earning the income.

- Do remember to attach all withholding tax statements when claiming actual taxes withheld from wages, salaries, or pensions. This is necessary for verifying the amounts claimed on the form.

- Do claim credits against tax that you are eligible for, such as the Family Tax Credit or Senior Citizen Tax Credit, if the income qualifying for these credits was earned by you.

- Don't include income or deductions not reported on your joint West Virginia tax return. The form should be a reflection of the joint return, with allocations made from there.

- Don't separate exemptions or claim part of an exemption. Understand that exemptions should be shown as they would be claimed by each spouse on separate West Virginia tax returns.

- Don't forget to allocate both additions to and subtractions from your federal adjusted gross income as per the guidance in the instructions for line 1 of the form.

- Don't neglect to allocate estimated tax payments correctly. Payments made by one spouse should be claimed by that spouse, while joint payments must be divided according to the form's instructions.

- Don't hesitate to consult a tax professional if you encounter difficulties or have questions about completing the form. It's important to ensure that every section is filled out correctly to obtain the relief sought.

By following these guidelines, filers can improve the accuracy of their WV 8379 form submission, aiding in the prompt and correct allocation of their West Virginia state tax refund.

Misconceptions

Understanding the WV 8379 form—West Virginia State Tax Department's Injured Spouse Allocation—can sometimes be challenging, and several misconceptions often arise regarding its use and requirements. Below are five common misunderstandings clarified to provide a better grasp of the form's purpose and process.

- Only one spouse's income is considered: A common misconception is that the WV 8379 form only accounts for the injured spouse's income. In reality, the form requires a detailed allocation of both the injured and the other spouse's income, taxes withheld, estimated payments, and allowable credits. This comprehensive data helps accurately calculate the portion of the refund that rightfully belongs to the injured spouse.

- It clears all debts: Some may mistakenly believe that filing Form WV 8379 will clear any debts owed by the other spouse that led to the refund being captured. However, the form's purpose is not to erase debts but to ensure that the injured spouse receives their fair share of the tax refund, which otherwise would be applied against the other spouse's outstanding child support or tax obligations.

- It's only for reporting joint income: Another misunderstanding is that the WV 8379 form is used solely for reporting joint income. While joint income is a component, the form also requires the allocation of various other items, such as additions and subtractions from federal adjusted gross income, exemptions, and various credits exclusive to either spouse. These details are crucial for correctly partitioning the tax liability and subsequent refund.

- Filing it guarantees a refund: Filing the WV 8379 does not automatically guarantee a refund. It's a common mistake to think that completion and submission of this form ensure the injured spouse will receive a refund. The actual refund amount is determined after the West Virginia State Tax Department reviews the allocation and computes each spouse's share based on the reported incomes, withholdings, and credits.

- It's only for correcting mistakes on the joint return: Some individuals incorrectly believe that the WV 8379 form should be used to correct mistakes or omissions on a joint tax return. While the form does involve detailing income and deductions specific to each spouse, its primary function is to allocate the joint return's refund between the spouses when one is not responsible for the other's debt. Therefore, it's not a tool for amending a return but for protecting the financial interest of an injured spouse.

Clearing up these misconceptions is critical for effectively utilizing the WV 8379 Injured Spouse Allocation form. It's designed to ensure fairness in the allocation of a tax refund when only one spouse has past due obligations that the state would typically offset against the couple's joint refund.

Key takeaways

The West Virginia 8379 form, also known as the Injured Spouse Allocation form, is designed for individuals who seek to claim their portion of a joint state tax refund that was seized or offset due to debts owed by their spouse. Below are key takeaways regarding this form:

- Eligibility for using the WV 8379 form requires the applicant to have reported income on a joint West Virginia tax return and to have part or all of their joint refund captured for the other spouse's past-due child support, back taxes, or other debts.

- The form allows both spouses to allocate joint income and deductions to compute each spouse's share of the tax liability, potentially reclaiming a portion of the captured refund for the injured spouse.

- Joint income includes, but is not limited to, interest from joint accounts and income from the sale of jointly owned property. The form necessitates the clear attribution of such income between the spouses.

- Each spouse's income, additions, and subtractions to the federal adjusted gross income reported on the West Virginia return must be clearly documented, following specific instructions provided for line items 1 through 3 on the form.

- While computing the allocation, exemptions that could be claimed by each spouse if they filed separate West Virginia tax returns must be reported without division.

- Taxes withheld from wages, salaries, or pensions are to be claimed exclusively by the spouse who earned the income. This also applies to taxes withheld from joint accounts and is important for accurately calculating each spouse's tax liability.

- Estimated tax payments and credits such as the Family Tax Credit or Senior Citizen Tax Credit should be claimed by the spouse who made the payments or who earned the income qualifying them for the credit.

- Line 8 specifically deals with West Virginia State or Municipal Use Tax reported on your joint return, requiring proper allocation between spouses.

- For non-resident or part-year resident filers, the form includes a section for allocating total West Virginia income from Schedule A based on who earned it, ensuring an accurate distribution of tax responsibilities and refund entitlements.

- Applicants must attach all relevant withholding tax statements to the form to support the allocation claims made.

Accurately completing the WV 8379 form is vital for ensuring that injured spouses can reclaim their rightful portion of a tax refund, providing essential financial relief in many cases. It’s important for individuals to carefully follow the instructions and provide thorough documentation to support their claims.

Popular PDF Forms

College Online Application - Acts as an official record for both scholarship application and academic performance, serving as a reference point for future academic endeavors.

Wv Sales and Use Tax Form - It outlines the tax exemption process for licensed carriers and government entities involved in aircraft operations.