Fill Out a Valid Wv 2848 Form

Navigating the complexities of tax matters with the West Virginia State Tax Department can be overwhelming for individuals and businesses alike. Fortunately, the WV-2848 form serves as a crucial tool to simplify this process. Officially known as the Authorization of Power of Attorney, this document allows a designated individual to act on behalf of the signer in specific tax-related situations. Given the sensitivity and specificity of tax affairs, completing this form accurately is paramount. It requires detailed information, including names, Social Security or WV Tax ID numbers, and contact details of both the authorizing individual (or business) and the appointed representative. Furthermore, it outlines the specific tax matters, such as type of tax, tax form number, and the tax periods concerned, to which the power of attorney applies. This power encompasses a variety of actions, including the handling of confidential tax information, signing tax returns and forms, and making agreements with the tax department. Significantly, the form also provides a mechanism for limiting or extending the authorized powers, thereby granting flexibility to address diverse needs. Such an authorization ensures that taxpayers can effectively manage their tax obligations through trusted agents, making the WV-2828 form a pivotal document in the realm of West Virginia’s tax administration.

Sample - Wv 2848 Form

Rev. 01/05

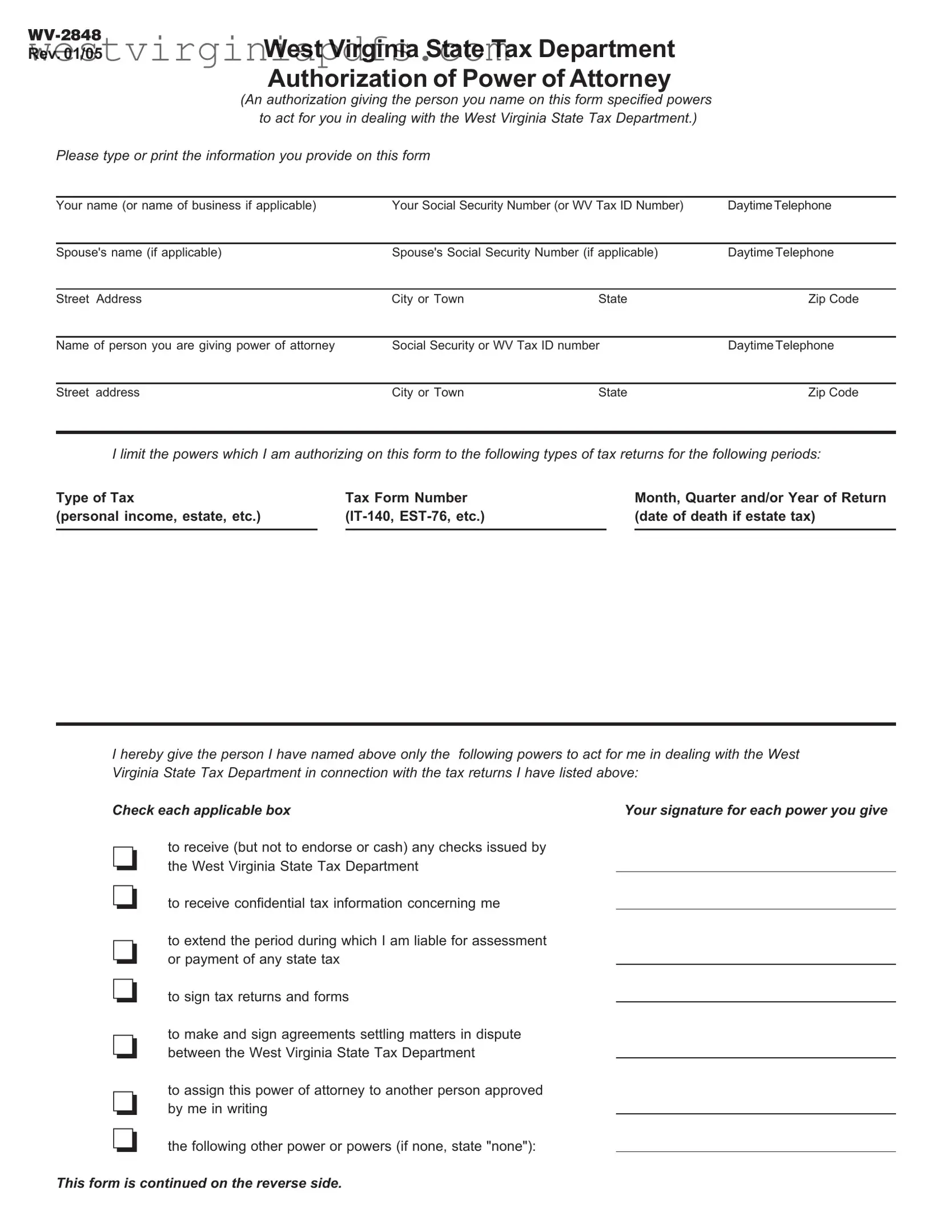

West Virginia State Tax Department Authorization of Power of Attorney

(An authorization giving the person you name on this form specified powers to act for you in dealing with the West Virginia State Tax Department.)

Please type or print the information you provide on this form

Your name (or name of business if applicable) |

Your Social Security Number (or WV Tax ID Number) |

DaytimeTelephone |

|

|

|

|

|

Spouse's name (if applicable) |

Spouse's Social Security Number (if applicable) |

Daytime Telephone |

|

|

|

|

|

Street Address |

City or Town |

State |

Zip Code |

|

|

|

|

Name of person you are giving power of attorney |

Social Security or WV Tax ID number |

Daytime Telephone |

|

|

|

|

|

Street address |

City or Town |

State |

Zip Code |

I limit the powers which I am authorizing on this form to the following types of tax returns for the following periods:

Type of Tax |

|

Tax Form Number |

|

Month, Quarter and/or Year of Return |

(personal income, estate, etc.) |

|

|

(date of death if estate tax) |

|

|

|

|

|

|

I hereby give the person I have named above only the following powers to act for me in dealing with the West Virginia State Tax Department in connection with the tax returns I have listed above:

Check each applicable box |

Your signature for each power you give |

❏the West Virginia State Tax Department

❏to receive confidential tax information concerning me

to extend the period during which I am liable for assessment

❏or payment of any state tax

❏to sign tax returns and forms

to make and sign agreements settling matters in dispute

❏between the West Virginia State Tax Departmentto receive (but not to endorse or cash) any checks issued by

❏

❏

to assign this power of attorney to another person approved by me in writing

the following other power or powers (if none, state "none"):

This form is continued on the reverse side.

I understand that in authorizing this power of attorney I am also giving the person I have named above the power to receive private and nonpublic information concerning my State taxes from the West Virginia State Tax Department.

I certify that no other person holds these powers for me. I understand that I have the right to revoke these powers at any time by notifying in writing both the person named above and the West Virginia State Tax Department.

This power of attorney revokes any earlier Authorization of Power of Attorney for the same types of taxes and periods covered by this power of attorney, but only to that extent.

Signature of or for taxpayer(s)

Your signature |

Date |

Daytime Telephone |

|

|

|

Spouse's signature (if any returns listed above are joint returns) |

Date |

Daytime Telephone |

|

|

|

Signature and title of corporate officer, partner or |

Date |

Daytime Telephone |

fiduciary authorized to execute this power of attorney on your behalf |

|

|

|

|

|

|

|

|

If the power of attorney is granted to a person other than an attorney or certified public accountant, the taxpayer(s) signature must be witnessed or notarized below.

The person signing as or for the taxpayer(s): (Check and complete only one of the following sections.)

❏is/are known to and signed in the presence of the two disinterested witnesses whose signatures appear here:

(Signature |

of |

Witness) |

|

(Date) |

|

|

|

|

|

(Signature |

of |

Witness) |

|

(Date) |

❏appeared this day before a notary public and acknowledged this power of attorney as a voluntary act and deed.

Witness:

(Signature of Notary)

NOTARIAL SEAL

(Date)

Mail to: |

West Virginia State Tax Department |

|

Revenue Division |

|

Post Office Box 2389 |

|

Charleston, West Virginia |

Document Specifics

| Fact Name | Details |

|---|---|

| Form Purpose | This form allows an individual to grant another person specified powers to act on their behalf with the West Virginia State Tax Department. |

| Form Number and Version | The form number is WV-2848, and the version is Rev. 01/05. |

| Type of Information Required | Information required includes personal or business name, Social Security or WV Tax ID number, contact details, and the types of tax returns and periods involved. |

| Applicability of Spousal Information | Spousal name and Social Security number are requested if applicable, particularly for joint returns. |

| Limited Powers | The form specifies that powers granted can be limited to particular types of tax returns and periods. |

| Types of Powers Granted | Powers include dealing with confidential tax information, signing tax returns and forms, extending liability periods, making settlement agreements, and more. |

| Option to Assign Powers | The form allows the appointee to assign the power of attorney to another person, with written approval from the original grantor. |

| Information Privacy Concern | Granting this power of attorney also permits the appointee to receive private and nonpublic information regarding the grantor’s state taxes. |

| Revocation Rights | The grantor reserves the right to revoke these powers at any time, through written notification to both the appointee and the West Virginia State Tax Department. |

| Witnessing Requirement | If the power of attorney is granted to someone who is not an attorney or certified public accountant, the taxpayer's signature must be witnessed or notarized. |

| Governing Law | This form is governed by the laws of the State of West Virginia and is specifically related to actions and transactions with the West Virginia State Tax Department. |

Guide to Using Wv 2848

The completion and submission of the WV-2848 form is a crucial step for individuals or businesses seeking to authorize a representative to act on their behalf in matters related to the West Virginia State Tax Department. It is a formal declaration giving specified powers to the named person, enabling them to handle tax affairs efficiently. This guidance is designed to help ensure that the form is filled out correctly and comprehensively, which is essential for the authorization to be recognized and acted upon by the relevant authorities. Here are the steps to follow:

- Type or print your full name or the name of the business if applicable in the designated space.

- Enter your Social Security Number (SSN) or WV Tax ID Number next to your name.

- Provide your daytime telephone number.

- If applicable, fill in your spouse's name, their social security number if applicable, and their daytime telephone number.

- Enter your street address, city or town, state, and zip code.

- In the designated area, write the name of the person you are giving power of attorney to, including their Social Security or WV Tax ID number, daytime telephone number, and their address information.

- Specify the types of tax returns, tax form numbers, and the month, quarter, and/or year of the return you are authorizing them to handle.

- Check each box next to the powers you are granting, which can include receiving confidential tax information, extending the liability period for tax assessment or payment, signing tax returns and forms, making and signing agreements, receiving checks from the tax department, and any other powers you wish to grant (if none, state "none").

- Sign and date the form to certify the authorization of power. Include your daytime telephone number.

- If there are joint returns listed, ensure the spouse also signs and dates the form, providing their daytime telephone.

- If the power of attorney is being granted on behalf of a corporation, partnership, or estate, the signature and title of the corporate officer, partner, or fiduciary authorized to execute this power of attorney on your behalf are required.

- If the power of attorney is granted to someone other than an attorney or certified public accountant, your signature must be either witnessed by two disinterested witnesses or notarized. Complete the applicable section.

After the form is completed, it should be mailed to the West Virginia State Tax Department at the address provided on the form. It's important to keep a copy for your records. The process of providing a power of attorney ensures that the designated individual can act on your behalf in a variety of tax-related matters, thereby potentially reducing the stress and complexity of dealing with tax issues directly.

Essential Points on Wv 2848

What is WV-2848 form used for?

The WV-2848 form, also known as the Authorization of Power of Attorney, is a legal document that grants an individual the power to act on your behalf in dealings with the West Virginia State Tax Department. Through this form, the person you designate will have the specified authority to handle tax matters for you, including receiving confidential tax information, signing tax returns, and making agreements concerning any disputes or liabilities with the state's tax authorities.

Who can I appoint as my Power of Attorney (POA) on this form?

You can appoint anyone you trust, such as a family member, friend, attorney, or certified public accountant, as your Power of Attorney (POA) using the WV-2848 form. However, if the POA is granted to someone who is not an attorney or certified public accountant, the signature on the form must be either witnessed by two disinterested witnesses or notarized to ensure its validity.

Do I need to specify what powers I am granting to my POA?

Yes, the WV-2848 form requires you to be very specific about the powers you are granting to your POA. You must check each applicable box in the form to indicate whether your POA is authorized to receive confidential tax information, extend the period for tax assessment or payment, sign tax returns and forms, make and sign agreements on tax disputes, and receive checks issued by the tax department on your behalf. You can also specify any other powers in the provided section if needed.

How can I revoke the Power of Attorney if I need to?

If you need to revoke the Power of Attorney given through the WV-2848 form, you must notify both the person you have named as your POA and the West Virginia State Tax Department in writing. The revocation will not be effective until the department has received and processed your written notice, terminating the authorized individual's ability to act on your behalf.

Does completing this form revoke previous Power of Attorney authorizations?

Yes, completing and submitting a new WV-2848 form revokes any earlier Power of Attorney authorizations for the same types of taxes and periods covered by the new authorization, but only to the extent that they overlap. It is important to accurately specify the types of taxes and periods your new POA covers to ensure there is no confusion regarding the revocation of previous authorizations.

Where do I send the completed WV-2848 form?

Once you’ve completed and signed the WV-2848 form, along with obtaining the necessary witness or notary public signatures if applicable, you should mail the form to the West Virginia State Tax Department at the following address: Revenue Division, Post Office Box 2389, Charleston, West Virginia 25328-2389. Sending it to the correct address is crucial to ensure that your Power of Attorney authorization is processed without delay.

Common mistakes

Filling out the WV-2848 form, an Authorization of Power of Attorney for dealings with the West Virginia State Tax Department, requires attention to detail and accuracy. However, individuals often make mistakes during this process. Understanding these common errors can help ensure a smoother process.

One common mistake is not fully completing the personal information section. Individuals must provide their name or business name, applicable Social Security Number or WV Tax ID Number, daytime telephone number, and address details clearly and completely.

Another frequent error involves the designation of the power of attorney (POA). When filling out the form, the name, Social Security or WV Tax ID number, and contact details of the person being granted POA need to be accurately filled in. Any inaccuracies here can lead to delays or a refusal of the authorization.

Many also err by not specifying the limitations of the powers granted. The form allows the granter to limit the POA's authority to specific types of tax returns for designated periods. Leaving this section blank or not clearly defining the limits can lead to unwanted or unauthorized actions.

- Not checking the relevant boxes to clarify the specific powers given to the POA is a common oversight. This includes the power to receive confidential tax information, extend liability periods, sign tax returns, and settle disputes, among others.

- Failing to sign and date the form is a critical mistake that renders the document invalid. Both the person granting the power and, if applicable, their spouse must sign and date the form.

- When the POA is granted to someone other than an attorney or certified public accountant, the requirement for the signature to be witnessed or notarized is often overlooked. This step is crucial for the validity of the document.

- Incorrectly handling the revocation of previous powers of attorney can also cause issues. This form automatically revokes any earlier authorization for the same taxes and periods, and acknowledging this is essential.

- Finally, sending the form to the wrong address or not sending it at all is a mistake that can easily void the effort put into completing it. The document must be mailed to the specified address of the West Virginia State Tax Department.

To avoid these common errors, it's vital to review the form thoroughly before submission, ensuring all sections are accurately completed and that the form is properly signed and dated. Paying close attention to the details can prevent unnecessary delays or complications in authorizing a power of attorney with the West Virginia State Tax Department.

Documents used along the form

When dealing with tax matters, especially concerning the West Virginia State Tax Department, the WV-2848 form, or Authorization of Power of Attorney, is a pivotal document. It authorizes a named individual to act on your behalf in dealings with the department. However, this form is often accompanied by several other documents to streamline the process and ensure comprehensive representation and compliance. Each of these documents serves a unique purpose, complementing the WV-2848 in the larger context of tax management and resolution.

- Form IT-140: This is the West Virginia Personal Income Tax Return form. It's essential for individuals delegating the authority to file or amend state income tax returns. The person granted the power of attorney may need access to this form to manage or scrutinize tax liabilities, file for the current year, or correct previous filings.

- Form EST-76: For estates subject to taxation, Form EST-76, or the Estate Tax Return form, becomes relevant. In situations where the power of attorney includes managing estate tax affairs, having access to, or the ability to file or amend EST-76, can be crucial for the proper settlement of the estate's tax obligations.

- Notice of Assessment: Often after filing tax returns, the West Virginia State Tax Department issues a Notice of Assessment, which details the taxpayer's liabilities, refunds, or credits. The individual with power of attorney needs this document to understand any outstanding liabilities or actions that need to be taken on behalf of the taxpayer.

- Form REV-1220: A Pennsylvania Sales Tax Exemption Certificate, contrasts with the WV-focused forms but may be necessary for businesses or individuals operating in both West Virginia and Pennsylvania. It exemplifies the need for authorized representatives to manage tax matters across state lines effectively, ensuring compliance and leveraging tax exemption benefits where applicable.

Understanding the role and requirement of each document related to the WV-2848 form minimizes errors and ensures that the person with power of attorney can act effectively on your behalf. Whether managing personal income taxes, estate affairs, or cross-state taxation matters, clarity and appropriate documentation are key to maintaining compliance and optimizing outcomes. It's important to consult with a tax professional to ensure that all necessary forms and documents are accurately completed and submitted in a timely manner.

Similar forms

The Internal Revenue Service (IRS) Form 2848, Power of Attorney and Declaration of Representative, bears significant resemblance to the WV-2848 form. Both documents serve to authorize another individual, such as an advisor or attorney, to act on the taxpayer's behalf in matters of tax. They specify the types of taxes and periods for which this authorization applies and allow for the designation of powers, including the signing of tax returns, receiving confidential tax information, and engaging with their respective tax departments (the IRS for Form 2848 and the West Virginia State Tax Department for WV-2848).

California's Form 3520, Power of Attorney, is another document with a similar purpose and structure. Like the WV-2848, it enables taxpayers to grant another person the authority to act on their behalf for state tax matters. These powers can include discussing tax matters with the state tax agency, receiving and responding to communications, and accessing confidential tax information. The specific nature of the tasks and tax types must be delineated in both forms.

The Uniform Power of Attorney Act (UPOAA) provides a general framework for power of attorney documents across many jurisdictions, and its influence is observed in the design of the WV-2848 form. Although the UPOAA covers a broad range of powers beyond tax matters, the principles of specifying the powers granted and the agent's responsibilities are reflected in the focused context of the WV-2848, emphasizing the importance of clarity and specificity in such legal authorizations.

The New York State Form POA-1, Power of Attorney, shares commonalities with the WV-2848 form in that it is designed to delegate authority for tax matters specifically within the state. This form includes options for appointees to perform a variety of tax-related tasks on behalf of the taxpayer, such as filing returns and communicating with the tax authority. Both forms also include safeguards to protect the taxpayer's interests, such as requiring notarization or witness signatures.

Form 8821, Tax Information Authorization, while not a power of attorney form per se, is closely related to the WV-2848 in its function to authorize individuals to receive a taxpayer’s information. Unlike the WV-2848, Form 8821 does not authorize the individual to represent the taxpayer before the tax authorities or sign documents on their behalf. However, both forms facilitate the sharing of confidential tax information with designated third parties.

The Medical Power of Attorney is an example of a document that, while differing in focus (healthcare decisions instead of tax matters), shares the underlying principle of authorizing another person to make decisions on one's behalf. The structure and intention behind the designation of an agent to act with specified powers under certain conditions reflect the fundamental nature of the WV-2848, illustrating the broad applicability of power of attorney in various aspects of personal affairs.

The Durable Power of Attorney for Banking Transactions and Safe Deposit Box Access operates within the financial realm, akin to the WV-2848’s domain in tax matters. It permits an appointed agent to manage the principal’s financial affairs related to banking. Despite the difference in application, both forms necessitate explicit designation of the agent's powers and scope, underscoring the essential nature of precision in the delegation of authority.

The Florida Department of Revenue's DR-835, Power of Attorney and Declaration of Representative, is tailored to tax representation within the state of Florida but parallels the WV-2848 in its provision for taxpayers to authorize representatives in dealings with the state's revenue department. Both encompass similar scopes of representation, including negotiation and settlement of tax disputes, submission and amendment of tax returns, and receipt of confidential information.

Advanced Healthcare Directive forms, although distinct in their healthcare focus, employ a similar conceptual framework to the WV-2848. These documents appoint a trusted individual to make healthcare decisions on the principal’s behalf under specific circumstances, mirroring the idea of entrusting someone with critical, detailed responsibilities in a highly personal context.

Last Will and Testament documents, which specify directions for estate administration after death, offer a conceptual parallel to power of attorney forms like WV-2848 by designating individuals to act on one's behalf. While addressing posthumous matters rather than tax representation, the principle of assigning responsibilities and authorities to trusted agents is a shared characteristic, underlining the importance of clear, deliberate assignments in legal arrangements.

Dos and Don'ts

When filling out the WV-2848 form, an Authorization of Power of Attorney for dealings with the West Virginia State Tax Department, it's important to ensure the information you provide is accurate and complete. Below are key dos and don'ts to guide you through the process.

Do:- Print or type information clearly to avoid any misunderstandings or processing delays.

- Provide all required personal details, including Social Security Number or WV Tax ID Number, ensuring they are accurate to prevent identity mismatches.

- Clearly indicate the specific powers you are granting to the attorney-in-fact, including types of tax returns and the periods they cover.

- Include the name and contact information of the person you are granting power of attorney to, verifying their details for accuracy.

- Sign and date the form to validate the authorization. If the form is for a business, ensure the appropriate corporate officer, partner, or fiduciary signs it.

- If applicable, have your signature witnessed or notarized, especially if the power of attorney is granted to someone other than an attorney or certified public accountant.

- Mail the completed form to the West Virginia State Tax Department at the provided address.

- Leave any fields blank. If a section does not apply, indicate with "N/A" or "none" to show you’ve acknowledged it.

- Grant more powers than necessary. Keep the authorization limited to what is truly required for the specific tax matters at hand.

- Forget to specify any limitations on the powers you are granting, including any specific tax forms or periods.

- Omit spouse's details if the returns listed are joint returns. Both spouses must sign the form when applicable.

- Overlook the option to revoke a previous power of attorney. Be clear if this form is meant to replace any previous authorizations.

- Forget to review and double-check all the information on the form before signing to ensure accuracy.

- Delay in notifying the West Virginia State Tax Department if you ever decide to revoke this power of attorney.

Correctly filling out the WV-2848 form will streamline the process of granting someone else the authority to handle your tax matters with the West Virginia State Tax Department, ensuring that your tax issues are managed effectively and according to your wishes.

Misconceptions

When it comes to legal documents, it's easy to get tangled in misunderstandings. The WV-2848 form, or the West Virginia Power of Attorney for the State Tax Department, is no stranger to misconceptions. Let's shed some light on four common errors people make about this form:

- It grants unlimited power. Many believe that by signing the WV-2848, they're giving away carte blanche authority over all their tax affairs. This isn't true. The form allows you to specify which powers you're granting, such as filing taxes, receiving confidential information, or even settling disputes. It's tailored to your needs and limitations.

- It can't be revoked. Another common misconception is that once the WV-2848 is signed, it's set in stone. This isn't the case. You have the right to revoke these powers at any time. Revocation must be done in writing and sent to both the West Virginia State Tax Department and the person you’ve granted power to on the form.

- Any type of tax return can be covered. While the form does cover a broad range of tax-related issues, it specifically requires you to list the types of tax returns and the periods they cover. It's not an all-encompassing document that automatically covers every type of tax or period. You must detail what you want the power of attorney to apply to.

- It automatically covers your spouse’s taxes. This is a crucial misunderstanding. If you're filing jointly, your spouse must also sign the WV-2848 form to authorize the same person to act on their behalf. The form separates authorizations for each individual, even in joint matters, ensuring that each party's tax matters are handled according to their own consent.

Understanding the specifics of the WV-2848 form can prevent unnecessary headaches and ensure that your tax matters are handled accurately and with your explicit consent. By debunking these myths, you’re better equipped to use this document to your advantage, granting the necessary powers while protecting your interests.

Key takeaways

Understanding how to properly complete and use the WV 2848 form, the West Virginia State Tax Department Authorization of Power of Attorney, is important for anyone looking to authorize another person to act on their behalf in tax matters. Here are key takeaways to consider:

- Type or print clearly when filling out the information to ensure all the details are legible and accurately recorded.

- Provide all required personal information, including your name (or business name, if applicable), Social Security Number (or WV Tax ID Number), and contact details. If this authorization involves a spouse, their information must also be included.

- Designate the authorized individual carefully, including their complete identification and contact information. This person will have significant authority to act on your behalf with the West Virginia State Tax Department.

- Be specific about the types of tax returns and the time periods you are authorizing the appointed person to handle. This clarity will help limit their power to only what you explicitly permit.

- Specify the powers you are granting by checking the appropriate boxes on the form. These powers can range from receiving confidential tax information to signing tax returns and settling disputes.

- Understand that by completing this form, you are also allowing the authorized person to receive private and nonpublic information concerning your state taxes from the West Virginia State Tax Department.

- Sign and date the form to validate it. If the authorization includes matters concerning a spouse or is on behalf of a corporation or partnership, the respective signatures are also required.

- A taxpayer signature needs to be either witnessed or notarized if the power of attorney is granted to someone other than an attorney or certified public accountant. This additional step ensures the authorization's legitimacy and your consent to it.

- To revoke the powers granted, you must notify both the West Virginia State Tax Department and the individual named in the power of attorney in writing. It's crucial to understand that this action will terminate the authorization moving forward.

By keeping these key points in mind, you can make sure that the WV 2848 form is correctly filled out and used according to your needs, offering peace of mind when delegating tax-related duties.

Popular PDF Forms

Hud Elkins Wv - Facilitates cross-referencing of legal information with other records, aiding law enforcement investigations and actions.

Wv S - This agreement empowers nonresidents to take control of their West Virginia tax obligations, thanks to the WV/NRW-4 form.