Fill Out a Valid Wv 103 Form

The WV 103 form, also known as the West Virginia Withholding Year End Reconciliation IT103 v.5, is an essential document for employers in the State of West Virginia, required to be filed with the State Tax Department, Tax Account Administration Division. This form plays a crucial role in the process of reconciling the amounts withheld from employees' wages for state taxes throughout the fiscal year. Employers must submit this form by January 31st following the end of the calendar year it pertains to, along with copies of all employees' Withholding Tax Statements (W-2s or approved substitutes). It serves multiple purposes, including verifying that the total tax withheld, as reported quarterly, matches the sum of taxes shown as withheld by all W-2 or 1099 forms issued by an employer. The instructions clearly outline the need for meticulous record-keeping and reconciliation between the total annual withholding reported and the individual withholding amounts documented per employee. Adjustments must be made if discrepancies exist between the total reported withholding and the aggregate amount from all W-2s and 1099s submitted. Moreover, it provides a mechanism for correcting underpayments or claiming overpayments, with stringent guidelines on how to proceed in either situation. The form underscores the significance of compliance with state tax regulations and the consequences of failing to submit the required documents or to meet electronic filing requirements for larger employers, highlighting the potential for penalties. For detailed instructions, electronic filing options, and additional guidance, employers are encouraged to utilize resources available on the State Tax Department’s website or to contact their support services directly.

Sample - Wv 103 Form

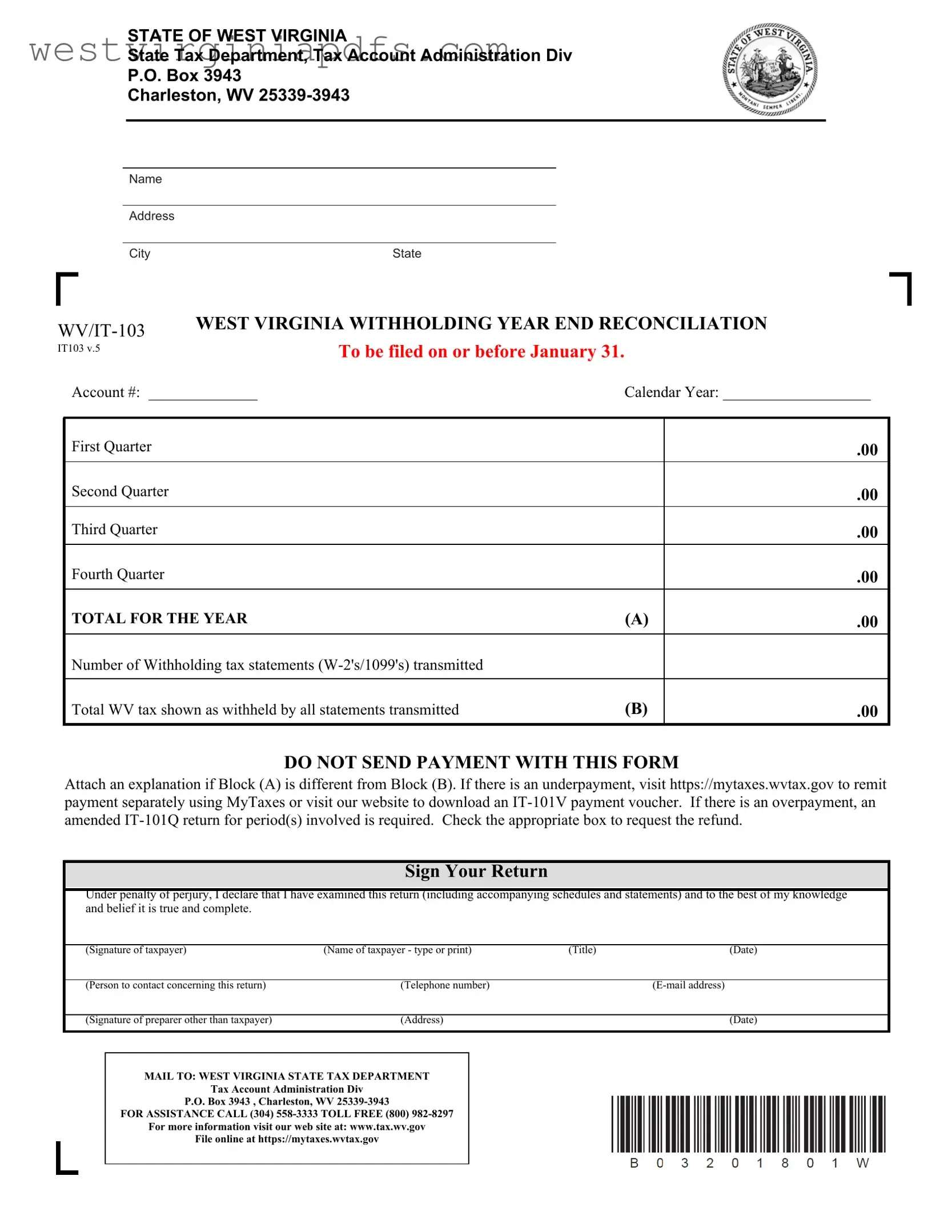

STATE OF WEST VIRGINIA

State Tax Department, Tax Account Administration Div

P.O. Box 3943

Charleston, WV

Name |

|

Address |

|

City |

State |

WEST VIRGINIA WITHHOLDING YEAR END RECONCILIATION |

|

||||

IT103 v.5 |

To be filed on or before January 31. |

|

|

|

|

|

|

|

|

|

|

|

Account #: ______________ |

Calendar Year: ___________________ |

|||

|

|

|

|

|

|

|

First Quarter |

|

|

|

.00 |

|

Second Quarter |

|

|

|

.00 |

|

Third Quarter |

|

|

|

.00 |

|

Fourth Quarter |

|

|

|

.00 |

|

TOTAL FOR THE YEAR |

(A) |

|

.00 |

|

|

Number of Withholding tax statements |

|

|

|

|

|

|

|

|

|

|

|

Total WV tax shown as withheld by all statements transmitted |

(B) |

|

.00 |

|

DO NOT SEND PAYMENT WITH THIS FORM

Attach an explanation if Block (A) is different from Block (B). If there is an underpayment, visit https://mytaxes.wvtax.gov to remit payment separately using MyTaxes or visit our website to download an

Sign Your Return

Under penalty of perjury, I declare that I have examined this return (including accompanying schedules and statements) and to the best of my knowledge and belief it is true and complete.

(Signature of taxpayer) |

(Name of taxpayer - type or print) |

(Title) |

(Date) |

(Person to contact concerning this return) |

(Telephone number) |

|

|

(Signature of preparer other than taxpayer) |

(Address) |

|

(Date) |

MAIL TO: WEST VIRGINIA STATE TAX DEPARTMENT

Tax Account Administration Div

P.O. Box 3943 , Charleston, WV

FOR ASSISTANCE CALL (304)

For more information visit our web site at: www.tax.wv.gov

File online at https://mytaxes.wvtax.gov

End of Year Reconciliation and Withholding Tax Statements

Employers are required to furnish each employee a Withholding Tax Statement (Form

Employees who are filing for

For additional information, please visit our website www.tax.wv.gov or contact:

Taxpayer Services Division

(304)

(800)

DO NOT ALTER YOUR TAX RETURNS INDICATING CHANGES

If there has been a change in your business please fill out this form by checking the appropriate box(es) and ensure your account number or EIN is indicated at the top of the form. Any change indicated on this form will be adjusted accordingly.

EMPLOYER'S WITHHOLDING CHANGE ORDER

Employer's Identification Number listed with West Virginia

**INDICATE CHANGES ONLY**

|

FEIN (WV State ID# if different) |

|

|

Filing Status |

|

Annual to Quarterly |

|

||

|

|

|

|

||||||

|

attach explanation |

|

|

|

|

||||

|

|

|

|

|

|

|

|

||

|

Business Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employer's Name (if different) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

City |

|

|

|

State |

Zip Code |

||

|

|

|

|

|

|

|

|

|

|

|

If you are no longer liable for West Virginia withholding tax, check explanation below; |

|

|

|

|||||

|

|

Business Sold Date Effective: ___________________________________ |

|

|

Business permanently discontinued Date Effective: ____________________ |

||||

|

|

|

|

||||||

|

|

Ceased paying wages Date Effective: _____________________________ |

|

|

Other - Specify: ________________________________________________ |

||||

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

Date |

Signature |

|

|

|

|

|

|

|

Mail to: WV State Tax Department PO Box 3943, Charleston WV

Page 2 of 2

Document Specifics

| Fact Name | Detail |

|---|---|

| Form Designation | WV/IT-103 West Virginia Withholding Year End Reconciliation |

| Filing Deadline | On or before January 31 |

| Governing Authority | State of West Virginia, State Tax Department, Tax Account Administration Division |

| Reporting Period | Calendar Year |

| Requirement for Employers | Must furnish Withholding Tax Statement (Form W-2 or an approved substitute) to each employee by January 31 of the following year |

| Electronic Filing Requirement | Employers filing for 25 or more employees must file electronically |

| Penalty for Non-compliance | $25.00 per information return not filed electronically |

| Underpayment Remedy | Visit https://mytaxes.wvtax.gov to remit payment separately or download an IT-101V payment voucher |

| Amendment Process for Overpayment | File an amended IT-101Q return for the period(s) involved |

Guide to Using Wv 103

Completing the WV/IT-103 form is a straightforward task that is essential for businesses at the end of the tax year. This document serves to reconcile the amount of West Virginia state income tax withheld from employees, ensuring that the total tax withheld matches the amounts reported on individual W-2 or 1099 forms. Timely and accurate completion followed by submission before the January 31 deadline not only keeps businesses in compliance with West Virginia tax regulations but also avoids possible penalties for late or incorrect filings. Below are the detailed steps for filling out the form.

- Enter the legal name of your business where it states "Name".

- Fill in the business "Address", "City", "State", and check the box for "WV" as the state symbol, confirming the form is for West Virginia.

- Input the "Account #" associated with your business's state tax account.

- Specify the "Calendar Year" covered by this reconciliation.

- Record the quarterly amounts withheld for taxes in the spaces provided for "First Quarter", "SecondWhile keeping variety in yourQuarter", "Third Quarter", and "Fourth Quarter".

- Enter the "TOTAL FOR THE YEAR (A)" by adding all quarterly amounts.

- List the total number of "Withholding tax statements (W-2's/1099's)" being transmitted with this form.

- Fill in the "Total WV tax shown as withheld by all statements transmitted (B)".

- If there's a difference between the "Total for the year (A)" and the "Total WV tax shown as withheld (B)", attach a written explanation.

- For any underpayment, follow the instructions for remitting payment separately, either via MyTaxes or with an IT-101V payment voucher. If overpayment is indicated, an amended IT-101Q return is required.

- Choose the appropriate option if requesting a refund due to overpayment.

- Sign the form in the provided space, indicating your agreement and declaration under penalty of perjury that all the information is complete and accurate. Include your "Title" and "Date".

- Provide a "Person to contact concerning this return" along with their "Telephone number" and "E-mail address".

- If someone other than the taxpayer prepared the form, have that individual sign at the bottom and include their address and the date.

- Finally, mail the completed WV/IT-103 form to the WEST VIRGINIA STATE TAX DEPARTMENT at the address provided at the bottom of the form.

After the form has been submitted, it's important to keep a copy for your records. Filing this form accurately and on time helps ensure that your business remains in good standing with West Virginia’s tax compliance requirements. For any questions or further assistance, the contact details provided on the form will direct you to the appropriate department within the West Virginia State Tax Department.

Essential Points on Wv 103

What is the WV/IT-103 form and who needs to file it?

The WV/IT-103 form, also known as the West Virginia Withholding Year-End Reconciliation, is a mandatory document for employers in West Virginia. It's used to report the total amount of state income tax withheld from employees' wages throughout the year. Any employer who has withheld West Virginia state tax from employee wages must file this form by the deadline.

When is the WV/IT-103 form due?

This form must be filed on or before January 31st of the year following the calendar year in which the income was withheld. For instance, for income withheld during the 2022 calendar year, the form would be due by January 31, 2023.

How should employers submit the WV/IT-103 form?

Employers are encouraged to file the WV/IT-103 form and upload W-2s online using the official website, https://mytaxes.wvtax.gov. Employers filing for 25 or more employees are required to file all data by electronic media. Further guidelines and specifications for electronic filing can be found on www.tax.wv.gov.

What information is needed to complete the WV/IT-103 form?

To accurately complete the form, employers will need their account number, a summary of the total wages paid, the number of W-2 and/or 1099 forms being transmitted, and the total West Virginia tax withheld as shown by these forms. Employers must also provide their business and contact information.

What happens if an employer fails to file electronically?

An employer who does not comply with the electronic filing requirement for 25 or more employees may face a penalty. This penalty is assessed at $25.00 per information return for which the employer failed to file electronically, emphasizing the importance of adhering to the electronic filing mandate.

Can I make a payment with the WV/IT-103 form?

No, you should not send payment with the WV/IT-103 form. If you find that there is an underpayment of tax, visit https://mytaxes.wvtax.gov to remit your payment separately using MyTaxes. Alternatively, you can download an IT-101V payment voucher from the website.

What should I do if there's an overpayment?

In cases of overpayment, you'll need to file an amended IT-101Q return for the period(s) involved. The form includes a section where you can check the appropriate box to request a refund.

Who can I contact for assistance with the WV/IT-103 form?

If you need help or have questions regarding the WV/IT-103 form, you can contact the Taxpayer Services Division at (304) 558-3333 or toll-free at 1-800-WVA-TAXS (800-982-8297). Assistance is readily available for those who seek it.

What if I need to report a change in my business details?

If there's been a change in your business, such as a change in business name, address, or employer's identification number, make sure to indicate this on the form. There is a section specifically for reporting changes, ensuring your business information is accurately updated in the state's records.

Common mistakes

Filling out the WV/IT-103 West Virginia Year End Withholding Reconciliation form is an essential task for employers, but it often comes with a handful of common errors. These mistakes can lead to delays, penalties, and added frustration during a process that is already quite meticulous. By paying attention to the finer details and avoiding these pitfalls, employers can streamline the procedure and ensure compliance with state tax regulations.

Incorrect or Incomplete Account Information: One of the first mistakes made is providing incorrect or incomplete account numbers and calendar year information. The account number is essential for identifying your business with the State Tax Department, and any errors here can misroute or delay the processing of your form.

Failing to Attach Required Documentation: It's crucial to accompany the WV/IT-103 form with all necessary W-2 and 1099 forms for your employees. Employers sometimes overlook this step, not realizing that these documents provide the detailed income and withholding information the tax department needs to verify the figures reported on the reconciliation.

Discrepancies between Totals: A common oversight is a mismatch between the total amount withheld for the year (Block A) and the total WV tax shown as withheld by all statements transmitted (Block B). These figures should match unless a legitimate discrepancy exists, which must be explained. Without a clear explanation for any difference, processing the form can be delayed while the discrepancy is investigated.

Neglecting to Sign the Form: Surprisingly, a simple but critical step that is often missed is signing the form. The signature attests that the information provided is accurate to the best of the signer's knowledge. In the absence of a signature, the form is considered incomplete and cannot be processed.

Ignoring Electronic Filing Requirements: For employers with twenty-five or more employees, WV/IT-103 forms and W-2 information must be filed electronically. Ignoring this requirement can result in a penalty of $25.00 per information return. This stipulation is often overlooked, leading to unnecessary penalties for the employer.

Understanding these common mistakes can help employers when completing the WV/IT-103 form. Meticulous attention to detail, thorough review of the form and attached documents, and adherence to filing requirements are key to a successful, penalty-free reconciliation process. By avoiding these errors, employers can contribute to a smoother tax season for both their business and their employees.

Documents used along the form

When filing the WV/IT-103 form for year-end withholding reconciliation in West Virginia, it is common for business owners or payroll professionals to encounter several additional documents that are either required or beneficial for a smooth and compliant filing process. Understanding these documents ensures that all financial and employee information is accurately reported to the State Tax Department, thereby avoiding potential penalties and ensuring the business's compliance with state tax regulations.

- Form W-2, Wage and Tax Statement: This form reports an employee's annual wages and the amount of taxes withheld from their paycheck. The WV/IT-103 form requires that a copy of Form W-2 for each employee be submitted alongside it.

- Form 1099: For independent contractors and other non-employees, the Form 1099 reports income that might not be subject to withholding but is still reportable for tax purposes. Similar to the W-2, copies of the 1099 forms must be submitted if taxes were withheld.

- IT-101V, Payment Voucher: Used for submitting payment for taxes owed to the state when they cannot be made electronically via MyTaxes or when accompanying a paper return. It helps ensure payments are properly applied to the correct account.

- IT-101Q, Amended Quarterly Return: If the WV/IT-103 form indicates an overpayment of taxes due to discrepancies in the quarterly filings, an amended IT-101Q form must be filed for each affected quarter, providing corrected information.

- Employer's Withholding Change Order: Although technically part of the WV/IT-103 document, this order form allows businesses to indicate changes to their withholding account, such as a change in filing status, business name, or address, or if the business is no longer liable for West Virginia withholding tax.

In addition to these forms, businesses should keep detailed payroll records and consult with the State Tax Department or a tax advisor to ensure compliance with current tax laws and regulations. Proper preparation and understanding of these forms can significantly reduce the complexities involved in filing and ensure that all procedures are completed efficiently and accurately.

Similar forms

The Form 941, Employer's Quarterly Federal Tax Return, is akin to the WV/IT-103 in that it is also a reconciliation document, but for federal rather than state taxes. Form 941 requires employers to report income taxes, social security tax, or Medicare tax withheld from their employees' paychecks. Additionally, it calculates the employer's portion of Social Security and Medicare tax, reflecting a similar need for periodic tax reconciliation to ensure the correct amount of taxes is collected and paid.

Form 940, Employer's Annual Federal Unemployment (FUTA) Tax Return, while focused on unemployment tax, shares common ground with the WV/IT-103 by requiring annual reporting from employers. This form is crucial for reporting the amount of unemployment taxes owed at the federal level, which is somewhat mirrored in the WV/IT-103's focus on withholding income tax obligations at the state level, showcasing the need for accurate annual tax reporting across different types of taxes.

The W-2 Form, Wage and Tax Statement, is directly related to the WV/IT-103, as it is one of the key documents summarized and reconciled through the WV/IT-103 form. Every employer must furnish their employees with a W-2 form, indicating the amount of money earned, as well as taxes withheld throughout the year. This information is then aggregated and reported on the WV/IT-103, demonstrating a crucial link in the chain of annual tax reporting and reconciliation.

Form W-3, Transmittal of Wage and Tax Statements, serves a parallel function to the WV/IT-103 by summarizing the information of individual W-2 forms and transmitting them to the Social Security Administration. Just as the WV/IT-103 accompanies the collective W-2 information for state tax purposes, Form W-3 does so on a federal level, further emphasizing the structured approach to tax documentation across various jurisdictions.

The 1099 Forms, particularly the 1099-MISC, are used to report various types of income other than wages, salaries, and tips. The relatedness to WV/IT-103 comes from the requirement that businesses report payments made to contractors or for other specific types of income, which then must be reconciled at the year's end, similar to how W-2 information is managed and reported through the WV/IT-103. Consequently, both forms play pivotal roles in the broader tax reporting and reconciliation process.

Form 945, Annual Return of Withheld Federal Income Tax, is utilized to report withheld federal income tax from nonpayroll payments, including pensions, gambling winnings, and backup withholding. Its similarity to the WV/IT-103 lies in its annual reconciliation of withheld taxes, though it focuses on a different subset of payments, underscoring the tax system's complexity and the necessity for multiple forms to cover various scenarios.

The State Unemployment Tax Act (SUTA) reporting forms, which vary by state, are also similar to WV/IT-103 in their function of reconciling taxes related to employment. While SUTA focuses on unemployment tax contributions at the state level, the principle of reporting and reconciling taxes based on payroll remains consistent, illustrating the nationwide practice of detailed employment tax tracking for governmental purposes.

The Quarterly Contribution Report and Multiple Worksite Report, often filed by employers in states to provide detailed employment and wage information for each of their operating locations, share the periodic reporting feature with the WV/IT-103. Although these reports may emphasize employment statistics more than tax amounts, the underlying goal of ensuring accurate records and payments to tax agencies is a common thread.

The Business Registration Certificate or License, required for operating legally in many states, is indirectly related to the WV/IT-103 form, as maintaining accurate tax records and filings, such as those documented on the WV/IT-103, can be crucial for retaining these certifications. Compliance with tax filing requirements reflects a business’s operational legitimacy and adherence to state laws and regulations.

Finally, the Amendment Returns for corrections of previously filed state tax documents bear similarity to the instruction on the WV/IT-103 regarding amendments for discrepancies. Should the amounts reported initially require correction, both form types provide a mechanism for businesses to rectify and submit accurate tax information, ensuring compliance with tax regulations and preventing future discrepancies in tax records.

Dos and Don'ts

Completing the WV 103 form correctly is important for both accuracy and compliance with state tax laws. Here are four things you should and shouldn't do to help guide you through this process.

Things You Should Do:

- Verify all information before submission: Double-check the taxpayer's name, account number, and all amounts reported on the form to ensure accuracy.

- Include all required attachments: Remember to attach explanations for any discrepancies between total yearly withholding (Block A) and the total WV tax withheld as shown by all statements transmitted (Block B).

- File by the deadline: Ensure that the form, along with any accompanying W-2's/1099's, is submitted on or before January 31 to avoid any late filing penalties.

- File electronically if applicable: For employers filing for twenty-five or more employees, use the electronic filing options available to save time and reduce errors.

Things You Shouldn't Do:

- Don't send payment with this form: If you owe additional taxes, make payments using MyTaxes or submit an IT-101V payment voucher separately, as no payments should be sent with this form.

- Don't guess amounts if unsure: If you're uncertain about any figures, it's better to verify the correct information through your records or seek assistance rather than risk errors by guessing.

- Don't wait until the last minute: Procrastination can lead to rushed mistakes or missed deadlines. Start the process early to give yourself plenty of time for review and corrections if necessary.

- Don't alter the Form to indicate changes: If there are changes in your business details, use the appropriate sections provided on the form rather than manually altering previously submitted details.

Misconceptions

When it comes to navigating state tax forms like the West Virginia WV/IT-103 Year End Withholding Reconciliation form, it's easy to get tangled in misconceptions. Let's clarify some of the most common misunderstandings:

The form is only for businesses that operate year-round. This is not accurate. Whether a business operates seasonally or throughout the entire year, if it has employees from whom it withholds state taxes, it needs to file the WV/IT-103 form to reconcile those withholdings annually.

WV/IT-103 is a payment form. This is a misconception. The form serves as a reconciliation document, not a payment form. It compares the total tax amount withheld from employees as reported throughout the year to the actual total tax amount transmitted. If there's an underpayment, payment should be remitted separately, and the form explicitly instructs not to send payment with it.

You must mail in your reconciliation. While mailing is an option, it's not the only one. The State of West Virginia encourages electronic filing and submission of W-2 forms through the mytaxes.wvtax.gov portal. This method is especially required for employers filing for twenty-five or more employees.

If there's an error, just correct it on the form and resend. Actually, altering tax returns to indicate changes is advised against. The correct procedure for businesses that have undergone changes (such as a change in address or business name) is to fill out a specific section on the form meant for indicating such adjustments.

Lack of forms is a valid excuse for late filing. The state does not consider lack of forms a valid reason for failing to file or late filing. It highlights the importance of understanding filing requirements and deadlines to avoid penalties, emphasizing the resources available on the state tax department's website for guidance and forms.

Electronic filing is optional. This might be misleading because, for employers with twenty-five or more employees, electronic filing of W-2 and 1099 forms is not optional but required. This mandate ensures efficiency and accuracy in processing large numbers of employee tax statements.

Understanding these aspects of the WV/IT-103 form can help businesses comply with state tax laws more effectively, ensuring that both the reconciliation process and reporting obligations are handled accurately and promptly.

Key takeaways

Understanding the WV/IT-103 West Virginia Withholding Year End Reconciliation form is crucial for accurate tax reporting and compliance. Here are key takeaways for navigating this form effectively:

- All employers are required to submit the WV/IT-103 form alongside copies of W-2 forms for each employee to the State Tax Department by January 31 of the following year.

- This form is designed to reconcile the total West Virginia tax withheld from employees as reported quarterly throughout the year versus the total reported at year's end.

- If there's a discrepancy between the total tax withheld during the year (Block A) and the total reported on W-2/1099 forms (Block B), employers must provide an explanation on the form.

- For underpayments, employers should not send payment with the WV/IT-103 form but instead use the online portal MyTaxes or download an IT-101V payment voucher from the State Tax Department website for separate remittance.

- If overpayment occurs, an amended IT-101Q return for the period(s) involved must be filed to request a refund.

- Employers who are filing for twenty-five or more employees must submit W-2 and 1099 forms electronically through the Tax Department's online system, failure to do so may result in a penalty of $25.00 per information return not filed electronically.

For assistance or additional information, employers are encouraged to contact the Taxpayer Services Division or visit the State Tax Department's website. Electronic filing via the MyTaxes portal not only streamlines the process but also ensures faster processing and reduces potential errors.

Popular PDF Forms

Wv Employee Withholding Form - Contains contact information for assistance, including phone numbers and a website for additional help.

West Virginia Auto Insurance Requirements - It allows residents of West Virginia to comply with the legal requirement of surrendering vehicle registration plates that are no longer in use.

Wv Court Forms - Advises on post-completion steps, including the submission of documents to fiduciary supervisors or county clerks, as appropriate, for the formal recording of the estate appraisement.