Fill Out a Valid West Virginia Cd 3 Form

Navigating the complexities of tax issues can indeed feel daunting, especially when it comes to settling tax debts with the state. The West Virginia State Tax Department's Offer In Compromise Form CD-3 shines as a beacon of hope for taxpayers looking to negotiate their state tax liabilities. Revised in April 2005, this crucial document serves as a formal proposition by the taxpayer to settle outstanding tax debts for less than the full amount owed under specific conditions. It details the taxpayer's name, address, and identification numbers, and requires a comprehensive list of the tax types, periods, and amounts due, including taxes, interest, penalties, and any additionals. The form outlines the total liability alongside the proposed settlement amount, stipulating the payment structure—initial, upon acceptance, and subsequent monthly installments. Critical to this negotiation process, the form includes clauses that prevent taxpayers from appealing the compromised liability amount, mandate the relinquishment of any refunds due until the offer amount is fully paid, and underscore the continuation of collection efforts if terms are violated. Furthermore, it stresses the suspension of the statute of limitations on assessment and collection while the offer is under consideration and for one year after all terms are satisfied, alongside a requirement for the taxpayer to remain compliant with state tax obligations for five years post-acceptance. A submission of this form not only requires a detailed explanation of why the offer should be considered but also necessitates attached financial statements and documentation to support the taxpayer's claims. With its stringent conditions and detailed requirements, Form CD-3 exemplifies the legal avenues available for individuals and businesses seeking respite from overwhelming tax burdens, aiming to balance the interests of the state with those of its taxpayers.

Sample - West Virginia Cd 3 Form

|

West Virginia State Tax Department |

|

|||

|

Offer In Compromise |

|

|

|

|

|

Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Names and Address of Taxpayer |

|

|

Taxpayer Representative |

|

|

|

|

|

Name: |

|

|

|

|

|

Address |

|

|

|

|

|

Phone |

|

|

Social Security or Tax Identification Number |

|

||||

|

|

|

|||

|

|

|

|

|

|

To: State Tax Commissioner |

|

Date |

Amount of Offer |

|

Total Liability |

|

|

|

$ |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

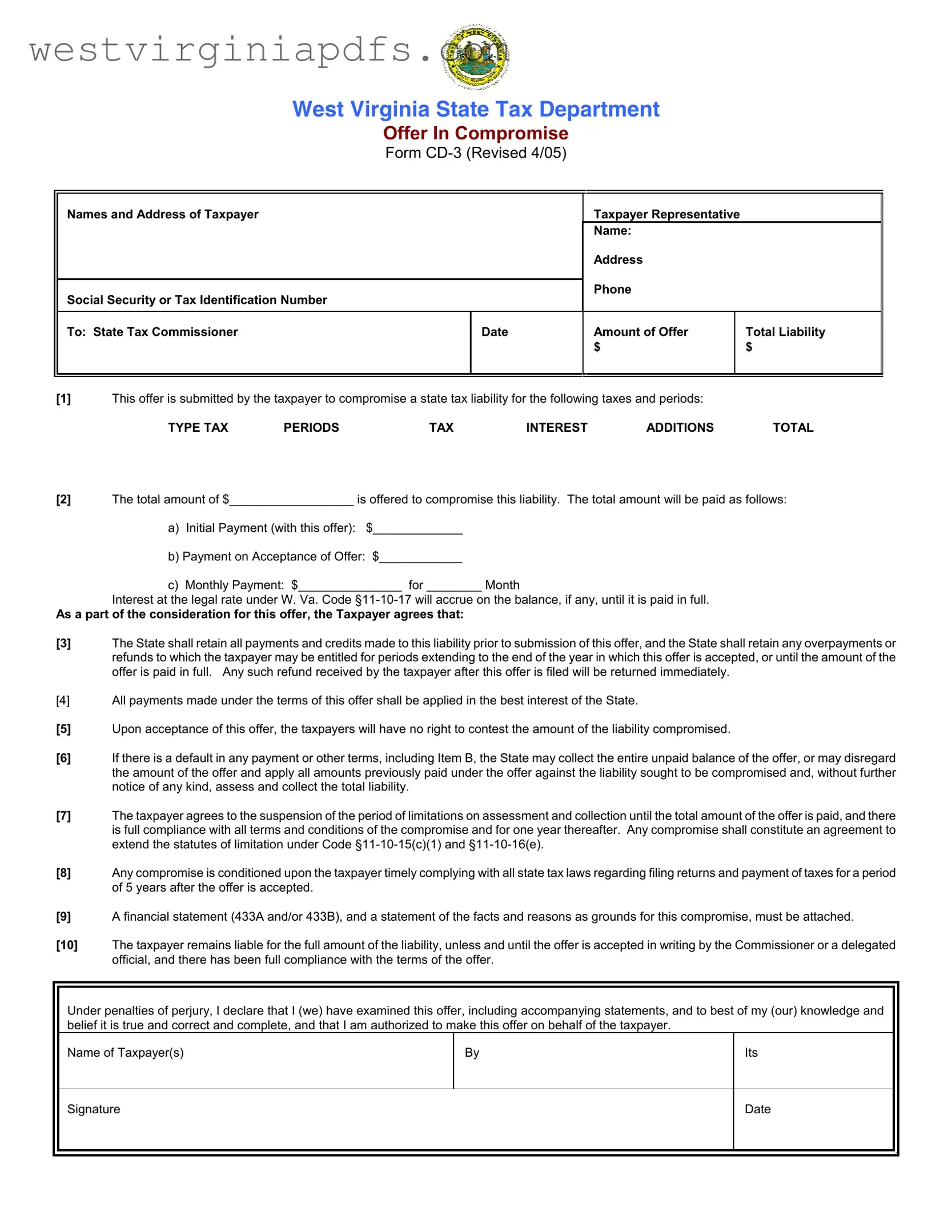

[1]This offer is submitted by the taxpayer to compromise a state tax liability for the following taxes and periods:

TYPE TAX |

PERIODS |

TAX |

INTEREST |

ADDITIONS |

TOTAL |

[2]The total amount of $__________________ is offered to compromise this liability. The total amount will be paid as follows:

a)Initial Payment (with this offer): $_____________

b)Payment on Acceptance of Offer: $____________

c)Monthly Payment: $_______________ for ________ Month

Interest at the legal rate under W. Va. Code

As a part of the consideration for this offer, the Taxpayer agrees that:

[3]The State shall retain all payments and credits made to this liability prior to submission of this offer, and the State shall retain any overpayments or refunds to which the taxpayer may be entitled for periods extending to the end of the year in which this offer is accepted, or until the amount of the offer is paid in full. Any such refund received by the taxpayer after this offer is filed will be returned immediately.

[4]All payments made under the terms of this offer shall be applied in the best interest of the State.

[5]Upon acceptance of this offer, the taxpayers will have no right to contest the amount of the liability compromised.

[6]If there is a default in any payment or other terms, including Item B, the State may collect the entire unpaid balance of the offer, or may disregard the amount of the offer and apply all amounts previously paid under the offer against the liability sought to be compromised and, without further notice of any kind, assess and collect the total liability.

[7]The taxpayer agrees to the suspension of the period of limitations on assessment and collection until the total amount of the offer is paid, and there is full compliance with all terms and conditions of the compromise and for one year thereafter. Any compromise shall constitute an agreement to extend the statutes of limitation under Code

[8]Any compromise is conditioned upon the taxpayer timely complying with all state tax laws regarding filing returns and payment of taxes for a period of 5 years after the offer is accepted.

[9]A financial statement (433A and/or 433B), and a statement of the facts and reasons as grounds for this compromise, must be attached.

[10]The taxpayer remains liable for the full amount of the liability, unless and until the offer is accepted in writing by the Commissioner or a delegated official, and there has been full compliance with the terms of the offer.

Under penalties of perjury, I declare that I (we) have examined this offer, including accompanying statements, and to best of my (our) knowledge and belief it is true and correct and complete, and that I am authorized to make this offer on behalf of the taxpayer.

Name of Taxpayer(s)

By

Its

Signature

Date

OFFERS IN COMPROMISE - INSTRUCTIONS

Authority

W. Va. Code

Reason for Compromise

We are allowed to compromise a liability for one or both of the following two (2) reasons: (1) doubt as to whether the taxpayer owes the liability; (2) doubt that we can collect the full amount of the liability. This form and instructions is only used in cases of doubt as to collectibility.

Policy

We will accept an offer in compromise when it is unlikely that we can collect the tax liability in full, and the amount offered reasonably reflects the amount we can collect. An offer in compromise is a legitimate alternative to declaring a case as currently not collectible or to a

The success of the compromise will be assured only if taxpayers make adequate compromise proposals consistent with their ability to pay the State. Taxpayers are expected to provide reasonable documentation to verify their ability to pay. The goal is a compromise which is in the best interest of both the taxpayer and the State. Where an offer in compromise appears to be a workable solution, the employee assigned the case will discuss the compromise with the taxpayer and, when necessary, assist in preparing the required forms. The taxpayer will be responsible for making the first offer for compromise.

Practical Consideration

It is the taxpayer's responsibility to show us why it would be in our best interest to accept your proposal. When we consider your offer we ask the following questions: (1) Could we collect the amount owed through liquidation of your assets or through an installment agreement? (2) Could we collect more from your assets and future income than is offered? (3) Would collection in the future result in more payment than is offered? (4) Would the public believe that the acceptance of your offer was a reasonable action?

The fact that you have no assets or income at this time from which the State could collect the liability does not mean that the State should simply accept any offer because it is all we can collect now. It would generally be better for us to reject a nominal amount and wait to see what collection potential would arise during the remainder of our

Additional Consideration

We believe that you benefit if we accept your offer because you can manage your finances without the burden of a tax liability. Therefore, we may require either: (1) A written agreement that will require you to pay a percentage of future earnings; and/or (2) A written agreement to give up present or future tax refunds.

Tax Compliance

(1)We will not accept your offer if you have not filed all tax returns. (2) We will also require that the taxpayer comply with all future filing and payment requirements. The terms of the offer require future compliance for a period of five (5) years.

Collection and Payments

The submission of an offer does not automatically suspend collection. If it appears the offer was filed to delay collection of the tax or that delay would hinder our ability to collect the tax, we will continue collection efforts. If you have agreed to make installment payments before you made the offer, those payments should continue.

Special Instructions for Offer in Compromise Form

(1)The Offer in Compromise form must be used to submit an offer. The form must be filed with the Compliance Division. If you have been working with a specific employee on your case, file the offer with that employee.

(2)Your full name, address and taxpayer identification number(s) must be entered at the top of the Offer form. If this is a joint liability (husband and wife) and both wish to make an offer, both names must be shown. If you are individually liable for a liability and are also jointly liable for another liability, and only one person is submitting an offer, only one offer must be submitted. If you are individually liable for one liability and jointly liable for another and both joint parties are submitting an offer, two (2) Offers must be submitted, one (1) for separate liability and one (1) for the joint liability.

(3)You must list all liabilities to be compromised in item (1). The types of tax, the periods, and the amounts must be specifically identified.

(4)The total amount you offer must be entered in item (2). The amount must not include any amount which has already been paid or collected on the liability. The amount submitted with the offer is entered in 2(a); the amount is to be paid on acceptance of the offer is entered in (2) (b) and any amount to be paid in installments, is entered in 2(c) in item 2. You should pay the amount of the offer in the shortest time possible, or we will reject your offer. Under no circumstances should the payment extend beyond two (2) years. Interest is due at the legal rate from the date of acceptance to the date of full payment.

(5)You must state in detail in item (9) why the State should accept your offer. Attach additional pages as necessary. Describes in detail why you believe the State cannot collect more than offered from your assets and your present and future income.

(6)The taxpayer(s) must sign and date the offer. If a person other than the taxpayer signs the offer, a power of attorney must be submitted with the offer.

(7)Form

What You Are Agreeing To

Please read the Offer in Compromise Form carefully so that you understand that you are agreeing to:

(1)The period for collection is suspended while the offer is pending, while any amount offered remains unpaid, and for one (1) year after all terms and conditions of the offer are fulfilled.

(2)You won't contest or appeal the amount of the liability if your offer is accepted.

(3)You give up of overpayments (refunds) for all tax periods through the year the offer is accepted, and until the amount of the offer is paid in full.

(4)The collection of the entire tax liability, if you do not comply with all the terms of the offer, i.e. payment, future compliance.

Document Specifics

| Fact Number | Description |

|---|---|

| 1 | The West Virginia CD-3 form is used for Offers in Compromise to the State Tax Department. |

| 2 | Governed under W. Va. Code §11-10-5q(c), it allows the State Tax Commissioner to compromise a tax liability. |

| 3 | Reasons for compromise include doubt as to liability and doubt as to collectibility. |

| 4 | Taxpayers must submit a detailed financial statement (433A and/or 433B) along with their offer. |

| 5 | Interest accrues at the legal rate under W. Va. Code §11-10-17 until the offer amount is fully paid. |

| 6 | Upon acceptance, taxpayers give up the right to contest the amount and agree to comply with state tax laws for five years. |

| 7 | Offers must include the tax types, periods, and total liabilities intended to be compromised. |

| 8 | The offer is conditional and requires full payment and adherence to terms for complete liability resolution. |

| 9 | The State retains any payments or credits made towards the liability prior to the submission of the offer. |

| 10 | The taxpayer must have filed all required tax returns and comply with future filing and payment requirements. |

Guide to Using West Virginia Cd 3

The West Virginia CD-3 Form is a document for taxpayers who want to propose a compromise to settle state tax liabilities that they might not fully afford. It provides a structured way for individuals or businesses to offer a settlement amount less than what is owed, under certain conditions. The form requires detailed information about the taxpayer's financial situation, the tax liability they are seeking to compromise, and the terms of their proposed payment. Understanding the requirements and accurately completing this form is crucial for the taxpayer's offer to be considered by the State Tax Department. Below are the step-by-step instructions to fill out the form correctly.

- Start by entering your full name, address, and contact information at the top of the form.

- Add the name, address, and phone number of your taxpayer representative, if you have one.

- Include your Social Security or Tax Identification Number.

- Specify the date you are submitting the offer next to "To: State Tax Commissioner".

- Under "Amount of Offer", fill in the total amount you are proposing to pay and the total liability amount.

- In section (1), list the types of taxes, periods, and amounts owed, including tax, interest, additions, and total liability for each.

- In the offered amount section (2), break down how you plan to pay the compromised amount including initial payment, payment upon acceptance of the offer, and any monthly payments you propose along with the duration of those payments.

- Read through the conditions (3) to (9) under which your offer is being made and ensure you understand each. These outline the state's terms, your agreement not to contest the liability once the offer is accepted, and other important details.

- Attach a detailed statement explaining why the State should accept your offer as indicated in item (9). Include additional pages if necessary.

- Sign and date the form. If someone is signing on behalf of the taxpayer, ensure a power of attorney form is attached.

- Complete and attach Form 433-A and/or 433-B as required, providing detailed financial information. Include all required documentation to verify the information provided on these forms.

Once the West Virginia CD-3 Form and all accompanying documentation are submitted, the State Tax Department will review your offer. This process includes evaluating your financial situation and the feasibility of the offered amount against the total tax liability. It's important to familiarize yourself with the implications of the offer, including what you are agreeing to in terms of payment, future compliance, and the potential suspension of collection activities. Make sure to keep a copy of all forms and correspondence for your records.

Essential Points on West Virginia Cd 3

What is the West Virginia CD-3 form?

The West Virginia CD-3 form is used for taxpayers to submit an Offer in Compromise to the State Tax Department. This form allows taxpayers to propose a settlement for less than the total tax liability they owe, including tax, penalty, interest, or additions to tax, under certain conditions.

Who can use the CD-3 form to make an Offer in Compromise?

This form can be used by any taxpayer who believes they have a valid reason why they cannot pay their full tax liability or if there is doubt about the collectibility of the debt. This includes individuals and businesses facing financial difficulties that prevent them from paying their tax obligations in full.

What are the reasons for filing an Offer in Compromise using form CD-3?

The State Tax Commissioner may accept an Offer in Compromise if there is doubt as to the collectibility of the tax liability or if there is doubt about whether the taxpayer actually owes the liability. The form and accompanying instructions are focused on cases where the amount of the tax liability is not in dispute, but the taxpayer's ability to pay is in question.

What needs to be included with the CD-3 form?

Along with completing the CD-3 form, taxpayers need to include a detailed financial statement (Form 433-A for individuals or Form 433-B for businesses) and a statement explaining the reasons for the Offer in Compromise. Taxpayers should also provide any additional documentation that supports their inability to pay the full tax liability or justifies the amount of the offer.

How should payments be structured in an Offer in Compromise?

The total amount the taxpayer offers to settle their tax liability must be specified in the form, excluding any amounts already paid. This can include an initial payment with the offer, a payment upon acceptance, and monthly payments thereafter. It's important to propose a payment plan that reflects the taxpayer's ability to pay, aiming to settle the debt in the shortest time possible, ideally not extending beyond two years.

What happens after the Offer in Compromise is submitted?

After submission, the Offer in Compromise will be reviewed by the State Tax Department. While under review, the period for collecting the tax liability is suspended. If accepted, the taxpayer will need to comply with the terms outlined in the agreement, including possible future payments or forfeiting tax refunds. Failure to meet these terms may result in the state pursuing the full unpaid tax liability.

Are there any requirements for tax compliance with an Offer in Compromise?

Yes, taxpayers must have filed all required tax returns and must comply with all state tax laws, including filing future returns and making tax payments, for a period of five years after the offer is accepted. This ensures that the taxpayer remains in good standing with the tax authorities.Can the submission of the CD-3 form stop collection activities?

Submitting an Offer in Compromise does not automatically halt collection activities by the State Tax Department. If the department deems that the offer was submitted to unduly delay collection, or if delaying collection could jeopardize the collection of the tax, they may continue with collection efforts.

What is the importance of the taxpayer's signature on the CD-3 form?

By signing the CD-3 form, the taxpayer—or their representative with a submitted power of attorney—declares under penalty of perjury that the information provided in the offer, including all accompanying documentation, is true, correct, and complete to the best of their knowledge. This signature is a critical part of the submission as it verifies the authenticity and seriousness of the offer.

Common mistakes

Filling out the West Virginia CD-3 form, an Offer in Compromise to the State Tax Department, is a critical step for taxpayers seeking to settle their tax liabilities. However, several mistakes can occur during this process, potentially complicating or nullifying the effort to reach a compromise.

One common mistake is providing incomplete or inaccurate taxpayer information. It is essential to enter full names, addresses, and taxpayer identification numbers accurately at the top of the form. In cases involving joint liabilities, such as those of a married couple, both names must be shown. Errors in this section can lead to delays or refusal of the offer.

- Not listing all liabilities to be compromised in item (1) is another mistake. Each tax type, period, and the total amounts of tax, interest, additions, and the total liability need specific identification.

- Failing to propose a total compromise amount in item (2), excluding any amounts already paid, complicates the assessment of the offer. The amount should be broken down into the initial payment, payment upon acceptance, and any installment payments, respecting the two-year maximum period for completion.

- Omitting detailed explanations in item (9), which requires a statement of facts and reasons for the compromise. This omission leaves the tax authority without a clear understanding of the taxpayer's inability to pay the full liability.

- Forgetting to sign and date the offer, as required in item (6), or not attaching a power of attorney when it is signed by someone other than the taxpayer, invalidates the submission.

- Not including the required Form 433-A, Collection Information Statement for Individuals, and/or Form 433-B for Businesses with the Offer in Compromise. These forms are crucial for providing a complete picture of the taxpayer's financial situation.

- Ignoring the comprehensive documentation support requirement for the information listed on Forms 433-A and/or 433-B, including verification of assets, encumbrances, income, and expense information, diminishes the credibility of the submitted information.

Attention to detail in completing the West Virginia CD-3 form and accompanying documents is crucial for a successful Offer in Compromise. Carefully reviewing all entries and attachments before submission can significantly increase the likelihood of acceptance by ensuring the proposal is clear, complete, and justifiable.

Documents used along the form

When dealing with the West Virginia CD-3 Form, often required for offers in compromise with the state tax department, several additional forms and documents may be crucial to support the process. These are integral for providing a comprehensive overview of the financial situation of the taxpayer, ensuring the state can make an informed decision regarding the compromise offer.

- Form 433-A, Collection Information Statement for Individuals: This form is necessary for individuals seeking an offer in compromise. It collects detailed information about the taxpayer's income, expenses, assets, and liabilities, providing a snapshot of their financial health and ability to pay the tax debt.

- Form 433-B, Collection Information Statement for Businesses: Similar to Form 433-A but designed for businesses, this form gathers comprehensive financial data about the business's operations. This includes income, expenses, assets, and liabilities, which help determine the business's capability to settle its tax debts.

- Power of Attorney (POA) Documentation: If a taxpayer is represented by a third party, such as an accountant or attorney, POA documentation must accompany the offer. This document authorizes the representative to act on behalf of the taxpayer in matters related to the offer in compromise.

- Tax Compliance Verification: Before the state considers an offer in compromise, it must verify that the taxpayer has filed all required tax returns. Documentation proving that all state tax returns are up to date must be included with the offer.

- Proof of Income and Expenses: Supporting documents such as pay stubs, bank statements, and bills are often required to verify the information provided in Forms 433-A or 433-B. These documents help the state authenticate the taxpayer's claimed financial status and evaluate their true ability to pay.

Ensuring all the relevant forms and documents are accurately completed and submitted with the West Virginia CD-3 Form can significantly enhance the likelihood of a favorable outcome. Taxpayers should pay close attention to the details requested in each form and secure the necessary documentation to substantiate their financial position, streamlining the state's review process and aiding in the swift resolution of their tax matters.

Similar forms

The West Virginia CD-3 Form is similar to the IRS Form 656, Offer in Compromise. Both forms are used to propose a settlement for tax liabilities under certain circumstances, such as doubt as to collectibility or doubt as to the accuracy of the liability. They require detailed financial information from the taxpayer to support the offered amount and include terms regarding compliance with future tax obligations.

Form 433-A, Collection Information Statement for Wage Earners and Self-Employed Individuals, and Form 433-B, Collection Information Statement for Businesses, are also similar to the West Virginia CD-3 Form. They are required as part of the offer in compromise process for the IRS and provide a comprehensive view of the taxpayer's financial situation. These forms help determine the taxpayer’s ability to pay the tax debt.

The Installment Agreement Request, IRS Form 9465, shares similarities with the West Virginia CD-3 Form by allowing taxpayers to propose a payment plan for their tax liabilities. While Form 9465 focuses on installment agreements, both forms aim to facilitate tax liability resolution when full immediate payment cannot be made.

The Application for Taxpayer Assistance Order, Form 911, offers relief similar to the CD-3 Form but is used to request help from the Taxpayer Advocate Service when experiencing significant hardship due to tax issues. Both forms are mechanisms for taxpayers seeking resolution when facing tax-related challenges.

The Innocent Spouse Relief Request, IRS Form 8857, although designed for a very specific situation, shares the common goal with the West Virginia CD-3 Form of providing taxpayers with a means to mitigate tax liabilities under certain conditions. Form 8857 helps relieve a spouse of joint tax responsibilities when fairness dictates so.

The Change of Address Form, IRS Form 8822, parallels the West Virginia CD-3 Form in administrative function. It is used for updating taxpayer information to ensure proper communication during and after the resolution process, an essential step for successful compromise or any tax liability resolution situation.

The Request for Transcript of Tax Return, IRS Form 4506-T, complements the West Virginia CD-3 Form by providing taxpayers and the administration with historical tax return information. This data can be crucial in substantiating the taxpayer's financial situation and validating the basis for compromise or other tax resolution strategies.

The Employer's Quarterly Federal Tax Return, IRS Form 941, is indirectly related to the West Virginia CD-3 Form in the broader context of tax compliance and liability resolution. Regular submission of Form 941 and similar forms helps prevent the accrual of tax liabilities that might later necessitate the use of forms like the CD-3 for resolution.

Lastly, the Application for Extension of Time to File, such as IRS Form 4868, shares a procedural similarity with the West Virginia CD-3 Form. Both forms provide taxpayers with a mechanism to address their tax obligations in a manner that differs from the standard process—Form 4868 by extending the filing deadline and CD-3 by compromising tax debt.

Dos and Don'ts

When filling out the West Virginia CD-3 form, it’s important to follow specific dos and don’ts to ensure your submission is accurate and complete. Here are key points to consider:

Do:- Read all instructions carefully before you begin filling out the form.

- Ensure all personal information is correct, including your full name, address, and taxpayer identification number(s).

- List all tax liabilities you wish to compromise, including the type of tax, the periods, and the total amounts clearly in item (1).

- Accurately calculate and enter the total amount of your offer in item (2), excluding any previously paid or collected amounts.

- Attach a detailed explanation in item (9) of why the State should accept your offer, including reasons why the State cannot collect more than the offered amount from your assets and future income.

- Sign and date the offer. If someone other than the taxpayer is signing, include a power of attorney.

- Include Form 433-A and/or Form 433-B as required, with all sections completed and necessary documentation to verify asset, encumbrance, and income/expense information.

- Leave any required fields blank. Incomplete forms may be rejected.

- Underestimate the importance of attaching a detailed statement in item (9). This is your opportunity to make your case for why the offer should be accepted.

- Forget to include the initial payment with your offer if one is required.

- Fail to keep a copy of the completed form and all attachments for your records.

- Attempt to negotiate terms that extend beyond two years for payment, as this may lead to rejection.

- Ignore the need for timely compliance with all state tax laws and filing requirements for a period of five years after the offer is accepted, as stated in the form.

- Make the offer without thoroughly reviewing your financial situation and ensuring that you can meet the terms offered.

- Submit the form without understanding that you're agreeing to specific terms regarding the suspension of collection, contesting the liability, and giving up rights to any refunds during a specified period.

Misconceptions

Understanding the West Virginia CD-3 form, an Offer in Compromise, involves clearing up some common misconceptions. This document is pivotal for taxpayers seeking to resolve tax liabilities under specific circumstances. The aim here is to clarify these misunderstandings to aid in proper usage and expectations of the form.

Misconception 1: Any taxpayer can utilize the CD-3 form to reduce their tax debt. In reality, the CD-3 form is specifically for situations where there is doubt regarding collectibility or the accuracy of the tax liability. Taxpayers must present significant proof of their inability to pay the full amount or question the amount owed.

Misconception 2: Submitting the CD-3 form automatically stops all collection actions. The truth is that the submission of an Offer in Compromise does not halt the State's collection efforts, especially if it's perceived that the offer was made to delay these efforts.

Misconception 3: The offer amount can include previously made payments towards the debt. When proposing an offer amount on the CD-3 form, any payments already made toward the tax liability should not be included. The offer should represent a new, additional amount towards settlement.

Misconception 4: The State Tax Department prefers prolonged payment arrangements over lump sum offers. Contrary to this belief, the Department encourages taxpayers to propose settlement amounts that can be paid in the shortest time frame possible, ideally as a lump sum, to reduce administrative burdens and resolve the liability swiftly.

Misconception 5: The taxpayer can designate how payments are applied. Upon accepting an offer, the State retains the right to apply payments in the manner most beneficial to the State, not necessarily according to the taxpayer's preferences.

Misconception 6: If the offer is accepted, taxpayers can later contest the liability amount. Accepting an Offer in Compromise means the taxpayer agrees not to dispute the compromised tax liability amount further.

Misconception 7: Filing a CD-3 form is a guarantee the State will accept any reasonable offer. In fact, each offer is subject to review, and the State Tax Department only accepts an offer if it reflects an amount that reasonably could be collected in full, considering the taxpayer's financial situation. The department is not obligated to accept an offer, even if the taxpayer believes it is reasonable.

The process of submitting an Offer in Compromise through the CD-3 form is designed to be fair both to the taxpayer and the State Tax Department. It provides a pathway to resolving tax liabilities under specific circumstances but requires careful consideration and understanding of the terms and conditions involved. By dispelling these common misconceptions, taxpayers can approach the process with a clearer understanding and realistic expectations.

Key takeaways

The West Virginia State Tax Department's Offer in Compromise Form CD-3 is designed for taxpayers seeking to compromise their state tax liability. This document outlines the procedure and requirements for making an offer to the state to settle tax debts for less than the full amount owed. Here are key takeaways about filling out and using the form:

- The form allows taxpayers to propose a settlement amount to cover all taxes, penalties, interests, or additions to tax due for specified periods.

- Payments under the offer may include an initial payment with the offer submission, a payment upon acceptance, and monthly payments, with interest accruing at the legal rate until the total offer amount is paid in full.

- Prior payments and credits made towards the liability will be retained by the State, and any tax refunds due to the taxpayer for periods up to the acceptance of the offer (and until the offer is fully paid) must be returned to the State.

- All payments are applied in the best interest of the State, and upon acceptance of the offer, the taxpayer waives the right to contest the compromised amount.

- If the taxpayer defaults on the offer terms, the State may either collect the unpaid balance or apply previously paid amounts against the compromised liability without prior notice.

- The compromise agreement includes a stipulation that the taxpayer must remain compliant with all state tax laws, filing returns, and payment of taxes for five years following the offer's acceptance.

- A detailed financial statement and a statement explaining the reasons for the compromise must be attached to the form.

- The taxpayer remains fully liable for the disclosed liability until the offer is formally accepted by the Commissioner or a designated official, and all terms of the offer have been fulfilled.

Moreover, submitting an offer in compromise does not automatically halt collection actions. Taxpayers are encouraged to continue making any agreed-upon payments during the review period. The form and accompanying documentation aim to demonstrate to the tax authorities why accepting the offered compromise serves the best interest of both the taxpayer and the State.

Understanding these aspects of the Form CD-3 process is vital for taxpayers considering an offer in compromise to address their state tax liability. It emphasizes the importance of full compliance with the compromise terms and provides a pathway for potentially reducing tax debts under specific circumstances.

Popular PDF Forms

Wv 2848 - Use of the WV-2848 form can be crucial for taxpayers unable to personally manage their tax affairs due to various reasons.

Physician Credentialing Checklist - For non-U.S. citizens, visa or work permit details are required, ensuring the practitioner's eligibility to work within the state.